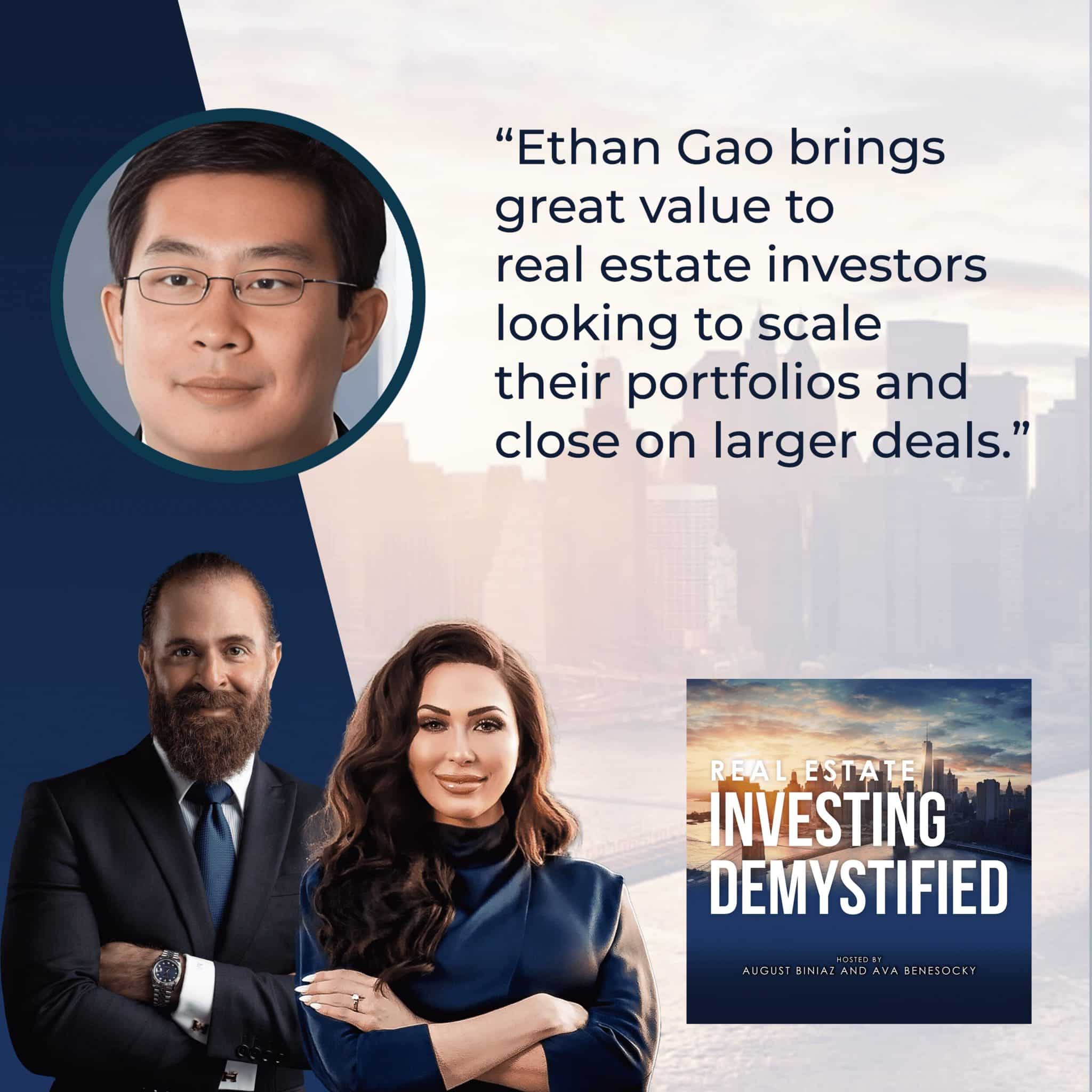

Are you a real estate investor looking to scale your portfolios and close more significant deals? Well, the Real Estate Investing Demystified has a treat stored for you! In this episode, Ethan Gao of Good Bull Investments explains how a Key Principal can help investors close larger deals. He takes us across his journey from investment banking to real estate and later on becoming a KP. He breaks down the role of a KP, providing clear scenarios for when they come in from his own experience and deals. As the conversation progresses, Ethan gives some insights about financial literacy, providing long-term strategies in this cyclical real estate market. To hear more of Ethan’s wisdom, tune in to this conversation now!

Get in touch with Ethan Gao:

LinkedIn: https://www.linkedin.com/in/elgao/

Website: https://goodbullinvestments.com/

If you are interested in learning more about passively investing in multifamily and Build-to-Rent properties, click here to schedule a call with the CPI Capital Team or contact us at info@cpicapital.ca. If you like to Co-Syndicate and close on larger deal as a General Partner click here. You can read more about CPI Capital at https://www.cpicapital.ca. #avabenesocky #augustbiniaz #cpicapital

—

Watch the episode here

Listen to the podcast here

Important Links

- RE Mentor

- Good Bull Investments

- Brice Scheschuk – Previous episode

- Rich Dad Poor Dad

- EthanGao@Gmail.com

- https://www.LinkedIn.com/in/elgao/

About Ethan Gao

Ethan is an attorney, Key Principal and General Partner. He has made over 300 private loans, invested in over 100 single-family fix and flips and is a general partner on multiple commercial and multifamily projects totaling over 900 units. His primary role on deals is loan guarantor/key principal or gap funder.

Ethan is an attorney, Key Principal and General Partner. He has made over 300 private loans, invested in over 100 single-family fix and flips and is a general partner on multiple commercial and multifamily projects totaling over 900 units. His primary role on deals is loan guarantor/key principal or gap funder.

Ethan personally and through his private equity fund, Good Bull Investments LP and Good Bull Lending, LLC has also invested in commercial properties totaling over $25 million.

Ethan graduated from Cornell University with a BA in Economics. Ethan was admitted to Columbia Law at 19 and graduated at 22. He worked on billion-dollar mergers and acquisitions for several years on Wall Street in financial institutions before transitioning to being a professional investor and entrepreneur in 2016. He lives in Houston, TX with his wife (who he met the first day of class at Cornell in 2000) and their five children.

Key Principal: How A KP Can Help Investors Close On Larger Deals With Ethan Gao

We are back at home and back at it. That was a great trip we had down to Arizona, Phoenix, and Tuscon, looking at a project we are working on. We were at an RE Mentor conference. It was great. There were close to 1,000 people that attended that conference.

Not a lot of people know this but conferences are a lot of work. You end up leaving those conferences feeling wiped. It’s hilarious. This one was three days of nonstop talking to people on your feet but it was a blast. We met some incredible contacts.

It was tremendous. We are back at it. We have a very special guest. I’m excited to have our guest here. I was preparing for the show. I know him personally but I watched a few shows that our guest has been on. I learned more about him. His background and credentials set the stage for who our guest is. Our readers would get a lot of value from our guests.

We were watching a couple of YouTube shows that Ethan has been on. It made me giggle. I have to share this with everybody. There’s a movie out there. It’s called Crazy Rich Asians. Somebody made a joke and said, “Crazy Smart Asians.” We’ve got a crazy smart Asian on our show.

I concur with that.

Let’s let everybody know a little bit about Ethan and then welcome him into the show. Ethan is an attorney. He’s a key principal and a general partner. He has made over 300 private loans invested in over 100 single-family fix and flips as a general partner on multiple commercial and multifamily projects totaling over 900 units. His primary role in deals is as a loan guarantor, a key principal or a gap funder. Ethan personally and through his private equity fund, Good Bull Investments LP and Good Bull Lending LLC, has also invested in commercial properties totaling over $25 million.

Ethan graduated from Cornell University with a BA in Economics. He was admitted to Columbia Law at the age of 19 and graduated at 22. He worked on billion-dollar mergers and acquisitions for several years on Wall Street in financial institutions before transitioning to being a professional investor and entrepreneur in 2016. He lives in Houston, Texas, with his wife, who he met on the first day of class at Cornell in 2000, and their five children.

Listening to that background, isn’t that the perfect child for Eastern parents? My parents are Eastern. You couldn’t have written it better than that. It’s like a dream child to have for Eastern and Western parents. Eastern parents are much harder on their kids than Western parents. If you tell your Eastern parents you want to become an artist, you might be in big trouble.

There’s one more thing. We believe this interview with Ethan is going to bring great value to real estate investors looking to scale their portfolios and close on larger deals. That’s enough of us talking. Ethan, welcome to the show. Thank you so much for being here.

Thank you so much. I was going to joke that the only thing that could have been better is if I was also a doctor.

Let’s start. We would love for you to tell us about your background and then your start in real estate.

I started on the traditional path. I come from a family of immigrants. We came to the US in 1989 and 1990. I was six and a half years old. I didn’t speak any English. The first year, I went through English as a second language and then graduated from high school when I was sixteen. I went to Cornell and decided I wanted to be a lawyer. I also didn’t think anybody would hire an eighteen-year-old college graduate anyway. I knew I wanted to go to graduate school. I went to law school and graduated in 2006 from Columbia Law School in a great economy.

We had multiple offers from good law firms in New York City doing mergers and acquisitions type of work. That’s what I did. My whole story is intertwined with my wife’s story. At Cornell, I met her on the first day of class. We have been together for many years. A couple of upperclassmen she knew did investment banking internships. They came back to campus and said, “Investment banking is great.” They make a lot of money. My wife said, “I’m going to do that.”

She had no idea what it was other than some smart people in her school who did it and told her that they make a lot of money. That’s why I went to law school in New York City so she could pursue her job in finance. She worked at JP Morgan doing investment banking for a couple of years. She got a job at a big private equity firm before she ultimately got an MBA from Harvard. We moved to Boston for two years and stayed there before we moved back to New York.

We moved to Hong Kong for a couple of years, from 2011 to 2013. We had our first kid in Hong Kong and then decided we needed to move back to the US. At that point, I was choosing between moving to Dallas or Houston. I happened to know someone in Houston who worked with me in the past. I was hired over a video conference in 2013 before this whole Zoom, the pandemic, and all that stuff. I got to Houston in April 2013. I have never been here before. I got off the plane. It was super hot. I realized I was in the right place.

Could you quickly describe what investment banking is? Maybe you can quickly give us a quick crash course on what investment banking is.

Investment banking is putting together deals, debt, equity, and the whole merger. What’s popular is Elon Musk trying to buy Twitter. He has to have investment banks that are going to provide him with the financing and the deal structuring. Investment bankers usually cover industries. You will specialize in industrials or something. Those people will always read about Honeywell or GE, what’s going on in those worlds, who’s merging with whom or who’s interested in selling what asset to whom. It’s more advanced real estate brokering.

Talk to us about your transition from investment banking into real estate.

I have always worked as a corporate lawyer. I worked a lot with investment bankers and stuff. I was never personally an investment banker, although my wife was. Those types of clients are always working on large deals all the time over the weekend and the holidays. As their attorney, we would also have to work over the weekends and holidays and do a lot of paperwork. A few years ago, I started investigating what I could do to not necessarily be in that world. The job was okay and the firm I worked at was fine but the nature of the is a tough job to do and advance with.

The joke that people like to make is that if it’s a pie-eating contest, once you win and you get promoted, the promotion is more pie. It’s a lot of stuff. I went down two paths to try to figure out how to exit that world. One was franchising. I researched a bunch of different franchises that I could buy. After doing due diligence, I determined that franchising was buying a terrible job. I figured I already had a job that I didn’t even have to buy. What’s the point of buying one?

The other line of things that I went through was real estate. I would constantly watch real estate podcasts and webinars and read real estate articles. What I found a little bit interesting was that the origin story of a lot of people in real estate is the exact opposite of mine. They are not immigrant Chinese households. These guys and gals were not that great at school. They had no money. They borrowed every penny. Now, they own 2,000 units across the country.

I kept thinking to myself, “If they are not even that good at school and didn’t start with any money, I’m great at school, and I already have millions of dollars on my own. Maybe I should try that.” That’s when I got into real estate. Specifically, I started by being a private moneylender. I wasn’t going to have the time or the expertise to buy a house cheap, fix it up, and sell it but I could figure out if somebody was doing that well and I could lend them the money for them to do that and charge them a high-interest rate. That’s what I did. That’s still what I do now.

Give us your thesis on private lending. In one of the shows that I watched, you talked about that. Fix and flippers are not going to hit jackpot on every deal that they do but as a moneylender, you are in a safe position. In the long-term, a private lender makes higher returns than someone doing fix and flips. Give us your thesis on that.

I’ve had the pleasure of having a couple of long-term borrowers who I’ve done a lot of deals with. With a gun to my head, I would bet you that what they paid me as their lender exceeded their overall profits in those ventures. Fix and flip is a tough cutthroat world. If you don’t buy it cheap enough, you don’t have a lot of room for error. It’s not particularly professional.

Fix and flip is a tough, cut-throat world. If you don't buy it cheap enough, you don't have a lot of room for error. Click To TweetThere are a lot of contractors that will steal money. If you time the market wrong, let’s say, you bought in March 2022 before all of the interest rate hikes happened. You had a large fix and flip. You had to do a lot of work. You try to sell it in December. You did time the market very poorly now that 30-year mortgage rates are 7%. When you bought it, they were at 4%. Now, they are at 7%. Your product is worth less.

That’s precisely why banks have been successful for centuries.

Lenders and landlords always get paid.

Somebody might be reading this and is like, “The person who’s doing the work, finding the property, doing the renovations, doing the value-add, and then flipping it, in the long run, might not make as much as the person who’s lending on the project.” There are a lot of these insane things that happen in business. For example, when I was in single-family construction development, there were individuals who got into the space, bought a piece of land, hired a builder, built a home on it, and then sold it.

When I did the calculation on it, if they had bought the piece of land and sat on it for the three years that it took for them to build and sell, they would have made the same profits. They didn’t have to go through all that headache. A lot of times, real estate is cyclical. Timing is very important. These strategies are long-term safe strategies. We are going to go over financial literacy and some of these strategies that exist later on but let’s keep going and talk about this important item that we are also in the midst of.

Let’s talk about it. Ethan, could you talk to us about your role as a KP? That’s also known as a Key Principal. What is a key principal? How do KPs help investors close on larger deals?

That’s my primary role in most of the deals I’m on. I don’t know exactly the history of this but it looks like it has been around for a while. When lenders go to make the loans, especially on multifamily syndication type of deals, they require that the lead sponsors have a net worth that exceeds the loan amount. It’s almost like a checkbox compliance item that has to be completed. I don’t know who invented this but it has been around for quite a long time.

It looks like the thesis from the bank is, “If this guy has a net worth that exceeds the loan, then the deal can’t possibly be that stupid. If something does go wrong, then this guy could sell some assets and still pay off the deficiency on the loan.” Let’s say we have a group and don’t have enough net worth. We would need to bring in someone that could help us augment the net worth and check the box.

In addition to that, the lenders typically require that 10% of the loan amount be shown liquid somewhere, even for people that have a high net worth. A lot of real estates investors have very high net worth but they have low liquidity. They also cannot check the liquidity box. They would need to bring in another person as well. In those situations, I am some other person. I get brought into those deals to help satisfy the liquidity and net worth requirements.

Is it fair to describe it as if somebody young or out of high school is looking to get a car loan and needs their parents to co-sign on it? Is it a similar concept?

Yes, it’s a similar concept. Sometimes the lenders will also focus on the key principal’s experience. I’m glad you brought that up. Sometimes somebody is young, just started, found a deal, and it’s a great deal but doesn’t have any real experience. That young person could have a high net worth and high liquidity. Let’s say they sold a tech startup or something. They still wouldn’t qualify. The lender would say, “Bring on somebody that has done this before.” Occasionally, experience level is also important. I’m on GP teams with over 1,000 units. Lenders want to see work experience in the field as well.

Without getting into the nitty-gritty and going too granular, there’s also a concept of recourse and non-recourse. Can you describe what recourse and non-recourse are and how they relate to being a KP? Is that an important factor when you are looking to invest or partner with other GPs on deals?

Thank you for pointing that out. That’s very important. What’s called a recourse loan is fully personally guaranteed by someone. I’ve done that before, especially with local banks here in Houston, on certain deals. A lot of local banks will only do recourse loans. What does that mean? I will give you an example. I’m on a couple of deals where we bought industrial land.

On those deals, there are small loan sizes because it’s just land but for some reason, let’s say that we can’t operate it very well and can’t get a tenant to rent it from us, and our maturity date comes due. That would mean that the bank could call me and say, “Ethan, remember that loan we made you a couple of years ago? You need to pay all of that to me.” That’s potentially risky if we don’t operate it well or if something happens.

A non-recourse loan, on the other hand, in that same situation with the industrial land, when the maturity date comes up, they might not be able to call me and say, “Ethan, pay the whole loan.” There are certain triggers that make it where they can do that. Those typically involve fraud and compliance. If we never turned in financial statements, some people call it Bad Boy Carve-Outs but that’s a little bit narrow.

It includes all the Bad Boy stuff like fraud but it also includes a bunch of compliance items like financial statements and insurance renewals. If you were doing your job, you should have done it on time but it’s possible that you may be super bad at financials or you could never find the right accounting firm, and you did not run a fraud but you could still be called to pay the whole loan.

That’s going to be rare. You would have to be incompetent to not be running a fraud and tripping these covenants. Hopefully, on any team that I’m on, we will not be that incompetent. We are certainly not going to do fraud but I would hope that we are not going to do anything incompetent where we can’t provide the compliance checks or the quarterly reporting.

To break this down a bit more, there are a couple of more questions here. Is it fair to say for yourself as a KP or Key Principal on deals that have been involved in recourse and non-recourse types of loans structured in that way that you would ask a group for bigger partnership shares in a recourse? This is more broadly speaking, not particularly with yourself but broadly speaking in the space when it comes to a key principal and a sponsorship team. Is it fair to say that projects and deals where the debt is structured as recourse are riskier and then, in turn, will demand a higher type of partnership shares or what have you?

That’s correct. They are riskier from a legal perspective. The bank could call and say, “You have to pay the whole loan off,” whereas in non-recourse, they can only do that if certain things or contingent triggers have been pulled. Another important thing to say is also when we report these loans on our balance sheet and the schedule of rules they own, a lot of banks will treat non-recourse loans as not debt but they will treat recourse loans as full debt.

Key Principal: The banks will treat recourse loans as full debt.

What that means is that some banks or lenders will calculate a global debt service coverage ratio even if we did the safest deal ever. We only borrowed 30% of the cost with 30% of the value but if that’s a full recourse loan, there’s going to be a lender or multiple lenders out there. When they do my global cashflow, they are going to assume that I have to pay the whole debt service myself with my legal practice or the fees I make from selling life insurance or something. That will also limit the total number of deals I can sign on.

I didn’t know that. That’s interesting. The last question on this before we move on is, on a deal where you’re a key principal, are you on that deal as a general partner and involved in decision-making and other aspects?

Typically, I would be included in the general partnership team. I wouldn’t be the lead operator or the co-lead operator. I would be more of a support role. If there are quarterly calls or updates, I would look at those but I wouldn’t be the one operating the property or anything like that. There have been a couple of deals where it has been more of a transaction-based situation. I don’t stay in the deal long-term.

I have one more question. As far as liquidity, having 10% of the liquidity other than cash, what counts as liquidity?

Stocks, bonds, and cash value life insurance count. I own a ton of life insurance. I’m worth a significant amount of money dead. If something happened to me, then go investigate that, please. There might have been a motive. I’ve had experience with being able to explain to lenders that my cash value life insurance policies count as liquidity. I’ve had no one push back on that, which is great. It truly is cash.

I have a checkbook that I can write checks against. It’s secured by my various life insurance policies. I have a very low-interest rate. The good thing for me is that it helps me manage my liquidity. Instead of having a couple of million dollars sitting around in cash all the time, earning a very low rate of interest, I have my money in my life insurance policies. Whenever I need that liquidity to fund something, then I write myself a check against my line of credit.

Key Principal: Instead of having a couple of million dollars sitting around in cash all the time, earning a very low rate of interest, I have my money in life insurance policies. Whenever I need that liquidity to fund something, I write myself a check against my line of credit.

Is it fair to say that you are a crazy smart and rich Asian?

I would hope so. I don’t know how smart and rich I am. I’m probably above average in both. Quite honestly, I would rather be a lucky Asian.

Let’s add that.

Luck is better. I met my wife first day of college. That’s luck. If I didn’t go to that college or if I didn’t graduate from high school when I was sixteen, I would have never met her, I wouldn’t have had five kids, and I might be way happier.

That’s great but I thought about it. If it weren’t for you coming in and making it more fun, the conversation would have been boring because I would have been thinking about analytics and other information.

I bring a lot of life to the party.

We were talking about private lending earlier but maybe we can describe private lending. It is debt. We want to do real estate deals and close on real estate deals. Debt is a huge part of our business leverage. When you compare how real estate has performed over the last few years to equities and other asset classes, real estate has done much better. That’s because of the leverage that exists in our business. Talk to us about private lending. Is there a situation where you don’t get involved? For example, you are coming in 3rd place as the 3rd mortgage, which is very risky. Talk to us about private lending. Do you come in the first place? Give us a crash course like you did earlier about KP and private lending.

The vast majority of the private lending I have done has been the first lien. Typically, these would be on single-family or fix and flips. Let’s say someone is buying a house for $100,000. They are putting in $40,000 of rehab money. They will sell it for $200,000. I would lend up to about 70% to 75% of the after-repair value of $200,000. My max loan would be $150,000. If I were lending them part of the rehab, they would have to do the rehab first and then get reimbursed through lender draws, escrow, and things like that.

It’s fundamentally a pretty safe proposition because if I lent $150,000 on a house that’s worth $200,000, houses aren’t super liquid but they are also not illiquid. You could get rid of it. In theory, if I sold it for $150,001, my whole investment was secure. Why do I care, especially if I can charge them 12%, 13% or 14% on the loan? That’s a great deal for me. I’ve done quite a few of those. I’ve also done several deals where I’m in second-lien positions.

On commercial deals here in Houston, I have one borrower, in particular, that’s very experienced. I have come in to lend him money on a second-lien basis which helps him to fully leverage his investment. He will get a bank loan for 70% of the cost, and then I will lend him about 30% as a second lien. He’s in the deal for $0 out of pocket but the reason I’m comfortable doing that is because of his experience level as well as because he is fundamentally able to buy deals cheaply. He’s buying stuff at $0.50 to $0.60 on the dollar. A third position would be rare. The third position is equity. I would probably joke and say, “Don’t even bother spending $50 to follow the lien.”

I’m excited to learn a little bit more about what is a gap funder.

I don’t want to say I invented this but I’m one of the only guys I know who talks about this at the networking events that I go to. I have been actively networking over the past few years to find opportunities to sign loans and be a loan guarantor. Through me talking about it all the time, one guy in July 2022 remembered that I hold a lot of liquidity.

He called me one day and said, “Ethan, I don’t need you to sign on a loan but I’ve got a friend that I’ve partnered with in the past. She needs $10 million of equity. She raised about $8 million. She’s short $2 million. Would you be interested in talking to her?” I said, “Why not?” We talked, and then I discovered this is a situation that we could lend money into. We would help out this person.

She would not lose her earnest money. She would get to collect her acquisition fee. Most importantly, she wouldn’t have to report to her investors. She has already raised $8 million. It’s sitting in her bank account. She wouldn’t have to go back, return all of that money, and then say, “I couldn’t close this one. I will call you for the next one.” You already know that if you do that on the next one, half of those people might not call her back because they will remember all that happened. They wired in a bunch of money, got it back, and didn’t make any money.

This helped her a lot. In exchange, I charged her interest on the loan that I made her and then got a position in the general partnership of the deal. That’s part of what I add to my unit count on my schedule at a real estate owned. Her repayment plan is short-term. I gave her 60 days to pay me back, so she had to continue fundraising to pay me back.

I like to describe it as a very expensive Band-Aid solution to get a deal closed. If I’m being a little bit more whimsical, my goal is to become your most expensive best friend for one day. As you reflect upon your life on your deathbed, if I wasn’t among the very handful of most expensive people you met, then I quite honestly didn’t charge you enough. I wish I could have charged you more.

You somewhat touched on the next question that I had. We know that brokers are an important part of business in general. If you want to buy real estate, you deal with brokers. If you want to sell real estate, you deal with brokers. If you want to get a loan, you deal with brokers. Brokers are very much involved even in a pref equity position where you are sourcing equity. You have your common equity. You want to fill in the gap. A pref equity position comes in either institutional or retail.

They come and fund that part of the stack. There are brokers involved for that part as well. Are there brokers involved when it comes to key principals? We could go and call up a broker, “Do you know any key principals that could assist?” Does such a service currently exist? Do you do your business through networking and building a brand around yourself?

As far as I know, there’s no service. There’s no Craigslist where you can post and say, “I will sign on loans up to $100 million.” I’m unaware of any of that. It’s mostly word of mouth. For whatever reason, people have asked for referral fees on this type of thing before but it doesn’t make a lot of sense. Referral fees make a lot of sense for listings or arranging debt, “I know a guy. You call that guy. Pay me 5%.” It’s hard to value what the thing is worth. You say, “If I’m getting 5% equity in this deal, then I will give you 5% of that. You get 0.25%.” It gets weird. Mostly, people don’t ask for that.

It’s not transactional.

It’s hard to say. There are some guys that have introduced me to people. They say, “Ethan, what do you need? What do you want?” They will try to arrange something with the borrower or the lead sponsor to get themselves in a position. In general, I found those to be less likely to work. A lot of that is a self-selection thing. The people that are super-duper concerned about how much money they are going to make by putting two people together are probably very greedy.

The people that are super-duper concerned about how much money they're going to make by putting two people together are probably just very greedy. Click To TweetDeals die because the other counterparty will see that versus somebody that says, “Call this guy. I don’t want anything.” Those deals are more likely to work out because you don’t have another third party trying to insert themselves in to try to collect money from as many sides as possible. We live in America and Canada. There’s nothing wrong with putting your hand out and making as much money from every side as possible. That’s what this country was founded on but sometimes, it doesn’t work.

I don’t want to bring spirituality into it, karma, and what have you but we are all brands. We were talking about the brand around you as someone who helps facilitate deals when it comes to debt, equity, and the most expensive best friend you could have ever had but without you, the deal couldn’t have happened. In life sometimes, when you build that brand around yourself, and you are adding value to others, even if it’s not being compensated, in the long run, it will come back and help you. That’s important.

Let’s touch on this last topic before getting to the next segment of our show. It is financial literacy. Listening to you speak, Ethan, and having known about you and being connected with you for a while, you speak a different language. You talk about finances and personal finance. Finance is different than most others do. You come from a finance background. You are a financial advisor, an active real estate investor, and a private lender. Maybe talk to us about your thesis on investing. We had a friend of ours, Brice Scheschuk, who runs a family office. He went in-depth talking about this. We learned a lot on that show.

Maybe you can talk to us about financial literacy. For example, should everybody invest in real estate? Give us the third crash course you are going to give us on financial literacy because you can’t go to school to be financially educated. There are so many different vehicles for investing. A lot of times, financial advisors talk about the world of equities and investing in index funds. They show proof that if you invested over the last 100 years, this is the type of return you would make.

“Put your money in index funds. Don’t do anything else. Sit back.” A lot of people subscribe to that ideology but I’m wondering. What is your thesis? If you were running a family office, and I have a feeling you will be in a short time, what would be your allocations? Can an individual use those same allocations that family offices, pension funds, and university endowments use? Overall, give us your idea about financial literacy and investing.

It’s not taught in schools very well at all. In general, probably a majority of the population has no business investing in anything. They should hand you their money. You will do the deal and then pay them distributions. They should do a little bit of due diligence about you, take a look at your deal, and then invest with a lead sponsorship team that’s solid. That would be better.

My team has a number of clients. A lot of them tend to be medical professionals like doctors who are constantly built out of money because one of their friends tells them about a great investment that’s going to be awesome. Here in Houston, there is a lot of oil and gas type of promoters. My joke about that is, “I don’t know a single person that invested in an oil and gas syndication that didn’t have a dry hole and lost all of their money.”

There are a lot of stupid investments that exist. The vast majority of people should probably invest in index funds, don’t look at anything, and wait until retirement. Another chunk should probably look for good lead sponsors with decent deals. There’s a smaller minority of people that should be very active in managing their money. I’m extremely active in managing my money.

I don’t invest as a passive investor or anything because I’m still at the age and the point in my career where I want to be active. There’s a lot of alpha to be generated by my being active. If I made $5 million a year as a senior executive at some company, I would 1,000% not be active with my money. I would probably put it all in the stock market and not bother or I would give it all to you.

Actively managing your money is a job on its own.

Sometimes it’s a scary job. In most jobs, if you screw it up, they continue to pay you for a while until they fire you. In this job, if I screw it up, I’ve lost my money. I feel like a moron. I didn’t get a paycheck and lost my money.

Most jobs, if you screw it up, continue to pay you for a while until they fire you. In this job, if I screw it up, I actually lose my own money. Click To TweetI appreciate it. I knew we were going to be to learn a lot on this show. We are going to go to the second segment of our show.

It’s the Ten Championship Rounds to Financial Freedom. I’m excited about this. It’s whatever comes top of mind. Here’s the first question. Who is the most influential person in your life?

My wife.

What is the number one book you would recommend?

I would recommend, Rich Dad Poor Dad. I read that when I was 21 years old. Someone told me about it. I threw it in the trash and said, “What is this guy talking about?” I read it again when I was doing real estate. I was like, “I shouldn’t have thrown that in the trash when I was 21.”

Rich Dad, Poor Dad

That’s the same story I had. I swear.

If you had the opportunity to travel back in time, what advice would you give your younger self?

Bet on the New York Giants that year that they beat the New England Patriots. They were 19-0. Bet on them. You would have made a lot of money.

A guy who’s done so well like Ethan, doesn’t need to give advice to himself. He’s like, “Keep doing what you are doing.”

This is a good one. What’s the best investment you’ve ever made?

It’s not financial. I was taking my wife out to dinner when I first met her. It only cost $12, and I’ve got five kids.

What’s the worst investment you’ve ever made? What lessons did you learn from it?

I had a friend that I ended up working for. I had an intermediate step between quitting my job and going full-time investments. This guy had it all. He came from a great family, spoke three languages very fluently and natively, and presented well but he was bad at managing his company. I saw a lot of red flags. A lot of it was negligence or recklessness.

I saw a lot of red flags but I still invested in that company because I worked there and believed in it. If I were ever to get another job, which I don’t expect to, I will tell my kids this. Let’s say they work at a tech startup or something. I would say, “That’s fine that you work there but don’t put your money in either. You are doubling down or tripling down on your risk.”

I’m interested in this question because it’s the perfect question for Ethan.

Ethan, how much would you need in the bank to retire now? What’s your number?

Do you mean that I don’t have to do any active investments?

It’s a trick question. It depends. We’ve got all kinds. How much would you need in a bank to retire? What’s your number? It’s up to you.

It’s low. I have extremely low expenses. I’m already at that point. A few million bucks are sufficient to retire. However, I enjoy what I’m doing. My kids are still pretty young. I quite honestly don’t want to spend the whole day with them. They can be extraordinarily annoying, especially when they are together. It’s not the age range where I want to go all in and spend the whole day with them. I’ve got several more years left where I have some time to create stuff.

I would hope that my kids are smart enough to realize that the stuff that I’m doing now is going to be more impactful to them versus me going to every camping trip, every baseball game or something like that. I would hope that they realize that what I did over the next couple of years is going to make a much bigger impact on their lives than me going to all their games.

If you could have dinner with someone, dead or alive, who would it be?

It probably would be with the guys that seem to be always at the right place at the right time or whoever bet on the Giants in 2007. I want to know what in the world they knew and how they were so confident to make large wagers on things like that, which look unpredictable because I feel like there’s a certain je ne sais quoi. There has to be something. There are some people that have it. You can’t describe it or know why. The guy that I told you about, who spoke three languages, presented well. I thought he had it but as I dig deeper, he didn’t have it at all. He had nothing. It was all smoke and mirrors.

Next question, Ethan, if you weren’t doing what you are doing, what would you be doing now?

I would be doing something very similar to this. I’m not creative enough to give you a great answer. I would not be a professional hunter or skateboarder. Those are not interesting to me at all. I would probably be more of a professional dad or I would still work as a lawyer. I come from a background where I always feel like I need to be working on something.

I don’t like to sit idly. These days, I can’t even watch TV without checking my email or working on something at the same time. It’s not the same. When I was younger, I used to be able to watch a full football game, have a bag of chips or something, and not move for a while but now, I have to be doing something while I’m watching the game. I can’t sit there and stare at the game.

How about a professional comedian?

I’m not witty enough.

Here’s my favorite question. Book smarts or street smarts?

You need a combination of both. I feel like street smarts are more important if you have to weigh them. Our team has had clients. We look at the investment they made. It’s like, “You invested in this because you are a doctor, and you make $900,000 a year. It doesn’t matter if you lose it all because you make it back the next year.” Some of these investments are horrible.

If they had street smarts, they would not have made the investment at all. Sometimes the best deals you do are the ones you don’t do. There are a lot of guys that are throwing their money into terrible deals. They should realize what their personality is and what they are enticed with. Either get professional advice or even better, stop investing. It’s not for everybody.

Here’s the last question. If you had $1 million in cash and you had to make one investment, what would it be?

I should probably say something like your education or something broad like that but I won’t say your education. Invest it into a gap loan. Between now and the end of the year, there are going to be people that have to raise a bunch of money to close because if you close on December 31, that is a material difference from closing on January 2nd or 3rd.

It’s not like, “If we close on October 29th or October 30th, who cares?” It’s because of the way our fiscal and calendar years run, December 31 is a real deadline that cannot be avoided in certain situations. My thesis is that between American Thanksgiving and New Year’s Day, a ton of people will be calling me to lend them millions of dollars to close their deals. I will be giving them the same story about how I need to be their most expensive best friend.

Thanks for that.

Thanks, Ethan. What’s the best way that people can reach you?

My email is best. I check my emails all the time unless I’m in a meeting or if I’m asleep. It’s EthanGao@Gmail.com.

We appreciate it.

Thank you.

Thank you so much for your time. We enjoyed this.

This was great. Thank you.