How do you build wealth? Is saving enough? Do you need to invest? Where should you be putting your money to achieve financial freedom? Here to answer your questions with wealth-building strategies is Brice Scheschuk. Brice is the Managing Partner at Globalive Capital and was previously Co-founder and CFO at WIND Mobile. He sits down with hosts Ava Benesocky and August Biniaz to offer tips to help you achieve financial freedom. Brice defines the importance of financial literacy, the compounding effects of saving, and the rich benefits of investing your money right. Tune in as he shares insights on how to manage your personal finance, and get started in building your investment portfolio. Don’t miss the wealth of knowledge from this episode and tune in for more money-saving and money-making tips!

Get in touch with Brice Scheschuk:

LinkedIn: https://www.linkedin.com/in/brice-scheschuk-cpa-ca-095721a/?originalSubdomain=ca

Website: https://www.globalive.com

If you are interested in learning more about passively investing in multifamily and Build-to-Rent properties, click here to schedule a call with the CPI Capital Team or contact us at info@cpicapital.ca. If you like to Co-Syndicate and close on larger deal as a General Partner click here. You can read more about CPI Capital at https://www.cpicapital.ca. #avabenesocky #augustbiniaz #cpicapital

—

Watch the episode here

Listen to the podcast here

Important Links

- Globalive Capital

- The Psychology of Money

- Antifragile: Things That Gain from Disorder

- Freedom Mobile

- Charlie Munger

- Farnam Street

- LinkedIn – Brice Scheschuk

- Twitter – Brice Scheschuk

About Brice Scheschuk

Brice Scheschuk is a Co-founder, Director and the Chief Financial Officer of Globalive Communications / Wind Mobile. He has been with Globalive / Wind for eight years in a senior finance capacity and is responsible for all aspects of finance, facilities and business planning including direct responsibility for raising in excess of $1.2 billion in capital.

Brice is the Co-President of Brave Investment, an investment holding company focused on private and public company and fund investing and manages over $10 million in assets across a number of investment classes including alternative funds, private and public equity, venture capital, angel, real estate, CPC’s, SPAC’s and RTO’s.

The Foundation Of Wealth Building Strategies – Foundations Of Building Wealth – Brice Scheschuk 2022

We have another great show for you. Please like and subscribe as it helps us build our channel and allows us to keep bringing you great content and expert guest speakers. Our mission is to empower investors to earn passive income through real estate investing. We’re excited because we are joined by Brice Scheschuk, a CPA and a Managing Partner of Globalive Capital.

He was the Cofounder and CFO of WIND Mobile as well as CEO of Globalive Communications. He has many years of experience building and operating companies at Globalive, Wind Mobile, Leitch Technology, and PricewaterhouseCoopers. He obtained his CPA and CA designation at PricewaterhouseCoopers and BCom Finance from Dalhousie University.

Brice served as a Marine Surface Officer in the Royal Canadian Naval Reserve. We believe that this interview with Brice will bring great value to anyone looking to learn about the fundamentals of personal finance, which are the foundations of wealth-building strategies. Furthermore, this interview will bring value to anyone looking to start or scale their company.

—

Thanks for being here, Brice. Welcome.

Welcome, Brice.

Thanks very much for having me, both of you. I’m delighted to be here.

Let’s start with financial literacy. What is financial literacy? Share with us the basics that anyone can use in their daily lives, please.

The classical definition of financial literacy is the ability to use knowledge and skills to manage financial resources for a lifetime of financial well-being. That’s an easy sentence, but there is so much in it that one has to consider societally and individually. Also, how we are doing, educate people, and think about this to move through what is one of the foundational issues in our lives and society.

The act of creating wealth, buying your house, and accumulating investment assets such that, in the future, you can retire, de-accumulate, and live a comfortable life. Have the insurance to protect yourself, pass along to the next generation, and all the complexity they’re in. For whatever reason, and there are probably many, we have not prioritized financial literacy, in my experience, in our education systems almost across the board, both in Canada and globally.

We’ve done ourselves a very big disservice as a society therein. These types of things, what we’re doing now, are examples of trying to move the ball forward on it. We’re seeing a lot of other resources coming because it is well recognized. What I say to people about that is that the first comment is you need to take ownership of your financial well-being. You do not want to rely on others, government, and social support. You want to own it, you can own it, and you have an opportunity to do that. That’s critical.

The last thing that I’ll say about this is there are some basic categories of financial literacy. It can be daunting when you’re not maybe a math person, or you haven’t done a lot of business and finance in your life. Quite frankly, the complexity of it is often done by an industry that benefits from complexity. I say to people that the goal is to simplify and simplify quickly.

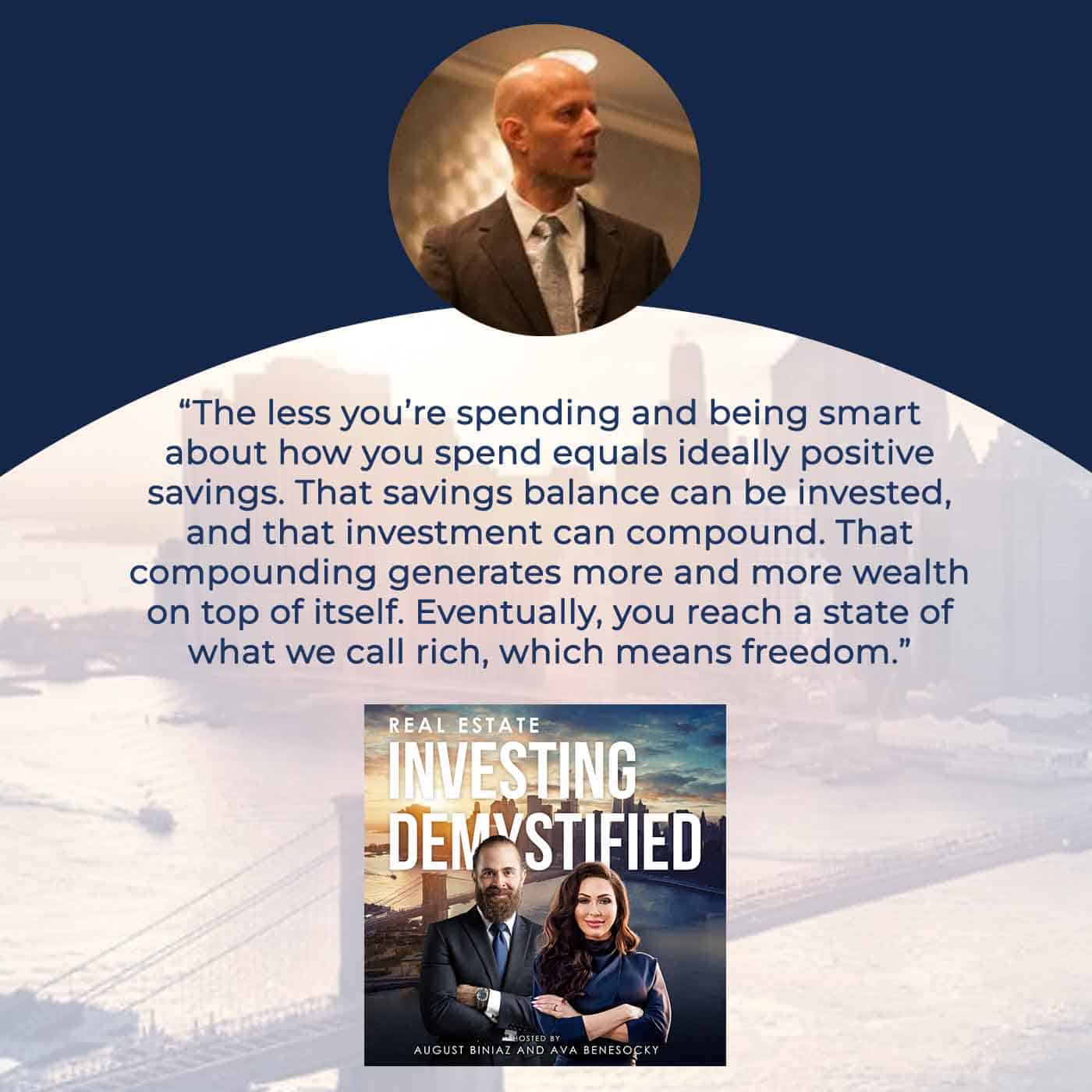

Think of it as how much you earn, the whole side of income, the job that you pick, passion, talent that you have, your income earning potential, and looking forward to the best industries. The less you’re spending and being smart about how you spend equals ideally positive savings. That savings balance can be invested. That investment can compound. That compounding generates more and more wealth on top of itself. Eventually, you reach a state of what we call rich, which means freedom.

Thank you for that, Brice. Let’s discuss the income and expense ratio, with the difference being savings. How can people increase their savings, and does increasing savings equal creating wealth?

It’s income, expense, net positive and negative. The income side is a more long-term thinking approach. Where do you pursue earning potential? How we break that up is we talk about a mix of where are your passion, talent and skills are, and where can you have an economic opportunity? We look at it as a bit of a triangle. An easy example that I always use is a good buddy of mine who is a soccer fanatic, but he recognizes that he doesn’t have the talent or the economic earning potential to be a professional soccer player. It’s an obvious simplified example. You want to get all three to work in sequence.

I’d like to use some terms like skate to where the puck is. We know what’s happening in society with innovation, technology, and the economy. We hear words like AI, Web 3, and self-driving cars. We look at Google, Microsoft, these companies, and the wealth creation that’s coming there. Those are great areas to look forward to when you think about your education, earning potential, and where to think forward. If I go to the spending side, the simple rule is to be careful when you move the goalposts. What we mean by that is simple. There’s a tendency when you add income, burn, and spending. Often, it’s not well managed.

As one is going up, the other is going up. You create a burn rate dependency that if anything happens on the income side, you have a real problem with maintaining your spending and/or you’re missing savings opportunities by doing some basic things like substitution. You then mentioned that is that net, if it’s positive, wealth creation? It is the start of wealth creation. You are creating something positive, and then you need to exercise it to the next phase, which is earning a return passively on that net positive savings.

This concept you speak about is the balance between smart investing and depriving yourself of life’s pleasures. How can this perfect balance be achieved? Let’s talk about that because I love this topic.

Perfection is always difficult, but I like where you’re going. I can give some directional examples. The one I use commonly is a silly example but it’s super illustrative. This is a true example. I’ve been lucky in life where I’ve had good employment and then have started businesses that have done reasonably well in the world. I’ve never been one who has to be super sensitive to spend.

The example I use is my wife, and I would go to Starbucks twice a day every day of the year for probably a decade. Two coffees a day, Americanos, lattes, and all that stuff. Let’s do some basic math. Starbucks, you almost can’t get out of there anymore without a $5 coffee. You do 4 of those a day across 2 of us. $20 a day, 365 days a year, and weekends, you name it, so it’s a little over $7,000 spent a year.

I went and bought a very nice machine to substitute for Starbucks. It gave me control of the beans. It gave me more control over what I wanted, like the convenience of having it at home. I cut my spend on an amortized basis from a little over $7,000 to about $400 a year. Stupid example, but $7,000 to $400, that $6,600 has now turned into an inflow to me that comes within an overall cashflow framework that can then start being invested.

This was probably when I was 23 or 24. If I could have those 10 or 15 years back of doing that, take that money, and compounded it by investing smartly, we would all fall off our chairs at how much money was left on the table. There are a few points to reiterate in that. Number one, don’t deprive. I have a better situation now than I used to with that Starbucks example.

Number two is to find smart substitutes, worry a little less about the status, and splurge every once in a while when you have to but watch that recurring behavior. Once you start doing a little bit of math on compounding and what that could mean for you from an investment standpoint, it becomes so addictive to change your behaviors a little bit to act on that compounding opportunity. That’s how I would explain it.

For anybody reading, compounding, research it because it’s a game-changer. Research that word and familiarize yourself with it and go after that compounding.

We’ve seen some of your past presentations where you show a slide that shows, “Would you rather have $1 million today or would you rather have $0.01 a day doubled?”

It’s way more powerful than that. I’ll give you a quick example. The first illustration of compounding is, would you rather have $1 million right now or $0.01 a day that doubles every day for 30 days? What you will find is that $0.01 becomes $0.02, $0.04, $0.08, and so on. In 30 days, that’ll be over $5 million. That is like my Starbucks example, although, sadly, my Starbucks example is true. That is a silly illustration of compounding.

Remember you said, is that wealth creation? What I find far more interesting is that if you can get that $1,000 of net wealth creation working for you quickly at a young age in some of these low-fee products, you set it and forget it and leave it. If you’re fifteen years old when you start it versus 20 or 30, the power at the back end of starting earlier is unparalleled. Your comment about learning about compounding is one of the 5 or 6 core principles that I would espouse. The concept added to learning about compounding is getting it put away, not thought about, and left for 30, 40, and 50 years.

It’s cool to show a fifteen-year-old the numbers so that they can get excited about it and start understanding them at a young age. The younger you start, the more you put yourself in a better position. I love what you said there. You talked about Starbucks with your wife, and you said, “We saved $6,600 a year. I could take that now and start investing.”

Let’s discuss investing. Should everyone invest? Is investing reserved for a selected few. I want to give an example. Our investments here at CPI are reserved for only accredited investors. This makes up 95% of the Canadian population and then 90% of the US population eligible to invest with us. Please talk to us about investing and if it’s the right strategy for everyone.

Great framing. Let’s put the concept of accredited and unaccredited towards the end of this. It is a super important concept to talk about. Let’s start with the common populace regardless of your station, accredited or unaccredited. The answer is a resounding yes. Everyone should invest. Let’s start there. One can’t be so blanket without some caveats.

Caveat one is there’s an exercise in life typically of incurring debt. I encourage debt incurrence only in two cases, the act of certain targeted student loans for an investment in yourself, being education. There’s a caveat to that. The second is for the purchase of housing in economies where the stock of housing makes sense to buy and becomes its own store of wealth, for lack of a better way to say it.

You need to take ownership of your financial wellbeing. You do not want to rely on others. You do not want to rely on government and social support. You want to own it and you can own it. You have an opportunity to do that. Click To TweetWhen you’ve incurred debt, there’s a debt servicing cost to that. It means that in the act of having positive net savings, you have a choice to pay down debt or invest. We won’t cover it here in any level of detail, but that is something that adds to the investment equation. The act of paying down debt for those types of things is a form of investing.

We then move solely to the act of investing. Let’s pick that easy example. Let’s use a very low-fee digital brokerage account example now. Pick a Wealthsimple, 100 other online brokerages, a quest trade, or whatever in Canada, Robinhood in the US, and a million others. If you can get $1,000 moving into there using North American numbers, not a third world or developing nations, and these are irrelevant to them as well, just on a divisible basis. If you can move money in there, set it and forget it.

Meanwhile, on the other side, your income and spending are being managed to create that small positive net savings you size your lifestyle accordingly. Getting that number working as early as possible in a global equity ETF gives you perfect diversification from Vanguard in one purchase at almost a zero fee.

You go away for 50 years and there’s an auto move from your bank account every month, $83 to get to $1,000 a year, and then it builds. I personally believe that everyone should do that. I will put a caveat. I understand that we have some social challenges and there are some deep poverty issues. There are circumstances. A small percentage of the population is in very difficult circumstances. That’s a social discussion that I’m not trying to cover here.

At least they should have the choice and know that the option exists.

What does all of that mean? I’ll tell you a few. Here’s what I think. The discipline of that creates a better earning and spending situation. You’re not always behind. The mindset of that is super powerful. We’ve talked about the act of compounding and early time working in your favor. The other thing is, once you start down that road, it forces you to get educated on the topics.

Because the education system doesn’t teach us effectively about financial literacy, they’re trying but they haven’t done a good job at it, it forces you to get yourself educated as early as possible in some of the basics, which is such a critical lifelong skill. That’s the mass comment I would make. It’s incredible for any middle-class person once they do a basic budget and look at their earnings and spending. Even kids with summer jobs, the examples I’ve used in other presentations, are smart savers. They’re living at home. They don’t have the same overheads. Start it and you won’t believe the discipline.

Let’s move to accredited-unaccredited. Here’s what I would say. There was a reason why they put the unaccredited-accredited rules in place. The regulators thought that they were protecting the common population from people selling investment products that were either unsavory or too complicated for them to understand. The entire regime of accredited and unaccredited should be revisited.

There’s a lot of thinking. You’ve seen the crowdsource and the crowdfunding rules allowing it to now be reached out to an unaccredited. There should be more allowance for unaccredited investing into more probably alternative and private and so on related products. It’s a disservice and a wide miss to wealth-generating opportunities, but we’ll leave that for a moment.

The comment I would make to you is all should invest, barring a few social comments, unaccredited done in a way that works within the system as low fee as possible and as technologically forward as possible. That phone we all have in our hands is the greatest thing ever from an investing and information standpoint. If you’re accredited, we start getting a little more complicated and sophisticated, but the fundamentals do not change.

Brice, what is the definition of being rich?

You’re teeing me up perfectly. You guys are younger than I am. I had status issues when I was younger. I was making okay money, trying to have the car, polo shirts, and all that kind of stuff. You realize when you get a little older and you can reflect on what means something. My definition of rich, which is well-trodden, is freedom. What is my definition of freedom? Unfettered control of time. Time is our most precious resource.

Every minute, every hour, every week, every month, and every year, you calculate how much you’ve got and how much you’ve got to be productive but also to have fun. I can’t believe I went from 25 to 50 and I don’t know how that happened. Time is the win. It all plays in a hierarchy. The control of time is achieved with passive income. The income from you not having to lift a finger to do anything is greater than your spend goalpost sized accordingly. That is my definition of rich.

When I was a little girl, my dad would always say, “As you get older, time goes by faster.” I never believed him. As I’m getting older, the value of time, in a blink of an eye, the days are going by. Well said. Thanks for sharing that.

That’s a wise father right there.

I want to switch the conversation a little bit here to building companies from the ground up. Brice, you’ve built some great companies. Please answer this question for me. Does a great company start with an idea or a team?

The short answer is usually a little combo of both but much more team. There are tropes that people talk about, 10% idea and strategy and 90% execution. Team and talent are always the number one criteria, particularly in the formation stage. Yes, that’s the answer. Here’s the thing that people get wrong. There is this view, “I don’t have good ideas on how to start a business. I haven’t had the a-ha moment. The light bulb never went off in the shower when I was thinking about my future.” The reality is, it never works that way.

What happens is that you live, work, do whatever, and start seeing problems that people are having, businesses, customers, consumers, or whatever it is. Those who succeed recognize that there’s a problem to be solved, and then they methodically start going about picking it apart and talking to people about the problem from the customer’s perspective. They start this flywheel of business building that iterates continuously to solve that problem better, faster, and stronger than whatever came before it.

Wealth Building Strategies: What happens is that you live, you work, you do whatever, and you start seeing problems that people are having. Those who succeed recognize that there’s a problem to be solved.

It’s not like, “I sat in the shower. Suddenly, Moses came to me with the Ten Commandments. Commandment number one is thou shalt build a new form of a rocket that travels supersonically in the world.” It’s much more an exertion business-building exercise, focused on the customer, finding the problem, and not creating a solution looking for a problem.

Our company was built on a problem that we’ve seen existed and we found a solution to that problem. We have big smiles on our faces because we can relate to that exact statement, and you’re correct in saying that.

It’s finding a solution to a problem and realizing there aren’t a lot of people offering the services for that solution. The problem was real estate prices were so high in Vancouver and Toronto, the main cities in Canada. They’re told all the time to invest in real estate. With medium-income being approximately $90,000 and medium home price being $1 million to $1.2 million, most people have a difficult time buying their primary residence. In some cases, they can even buy a rental property but to scale as real estate investors is difficult. To allow these alternative investments that CPI provides is something that we feel we solved as a problem.

We found a solution to a problem.

We’re not going to get into the detail of asset allocation and security selection. Back to your comment around the accredited and unaccredited, we believe that real estate is a cornerstone asset for all portfolios, generically. When we do our investing, we have a targeted asset allocation to real estate. Thankfully, we are accredited, so we have a relatively sophisticated way of looking at how to deploy within that category smartly.

What I hope happens, partly for your sake but also for the world, is that these accredited unaccredited rule changes happen whereby I’m the person saving $10,000 a year compounding, and I can go to you guys and do a $1,000 allocation or whatever makes the most sense in that context. I get a nice diversified portfolio of fractionalized ownership and real estate in whatever category within that narrative. You are finding a problem that exists. You are providing a solution. I hope your “addressable market” gets a lot wider as the regulators get a lot smarter.

That would be incredible. At CPI Capital, we’ve built a real estate private equity firm from the ground up. Now that our company is growing, we’re having discussions internally and we’re contemplating either hiring or bringing on partners. What is the better route, in your opinion?

When you say bring on versus hiring, do you mean more on a consultative basis, like under contract? How do we think about that?

Giving up a piece of the company where we don’t have to pay a salary then and hire the great minds we want to hire, but rather bring on a partner to give up a portion of our company. It is a struggle that a lot of newer companies go through in the early stages.

The short on it is what we see in the general innovation and technology forward, not the Subway franchisee who needs to bring on some counter staff. You’re talking about bringing in an A-player talent that is going to help drive your business forward and create wealth for everyone. In those scenarios, if that’s what we are talking about, unequivocally, if you look at the market now, we are in a complete and utter war.

Real estate is a cornerstone asset for all portfolios. Click To TweetYou’ve heard the term war for talent, the Great Resignation, people being able to take a step back because of the pandemic and think about what it is they want out of life and work. It’s changing the nature of work. That has, I would suggest, exacerbated what was already a trend in innovation-forward companies whereby equity is almost a must.

Equity means a few different things. We should drill on that for a minute. There is an employee where you bring them on. They’re A-player talents. You’re going to pay them a salary because they do need to live and issue them maybe some stock options as an equity incentive that best over time to have them invested in the business. Think about the company every day and charge forward, knowing that wealth creation is happening beyond the salary that they’re getting. That is one form of equity.

The other form is you’re probably looking for a partner that would be a little more established. They would have wealth and interest and skill in what you’re doing. They would say, “I want to buy 20% of your company. Set a value. I’m going to put money in.” One of your asks is, “I want you to come in as an advisor or a board member.” Going to the extreme of employment is not unknown. It’s maybe a little less practical when they’re wealthy and can afford to buy in. It’s like, “We want to build this thing together and figure it out.”

If I could summarize to try to shorten the conclusion here. There is an employee-style equity incentive, which is a necessity in nimble small innovation-forward companies to get A-talent. There is the act of selling a part of your company for cash that then turns into what is the relationship you will have with that capital provider as an advisor, management team member, cofounder, or board member that helps you propel the business forward. That’s generally how I look at it.

That leads to the next question, who should be the first person a company hires aside from the original founders?

It’s generalized, so it’s hard to answer it perfectly. I can tell you the personas and what I generally see. When we think about innovation, we break it into three personas of people in a company. One is the builder. Call it the product or the technology, that whole world of creation. Number two is the seller. It’s that person who we all know who’s a networker, who goes out and talks to the customer, who’s talking to partners, and who’s always drumming up the next thing, that outgoing type personality.

Number three is what we call the measurer, which is more of that finance, operations, making sure the donuts are made every morning, and everything is working on time. It’s too hard to generalize, but I would say that finding out where your weaknesses are as a founding team is often where I look to fill first.

I’ll give you an example. In technology, what we see a lot is technical teams coming together, a bunch of very smart engineers. They have this problem that they’re solving and they start building a product. They then need to think about customers. None of them know how to sell or how to talk to customers. Very frequently, an early hire is what they call a go-to-market, a chief revenue officer, a sales, marketing, or whatever that world is.

You can also see the flip where you have some great salespeople that come together. They don’t know how to build technology and need a tech hire to come in and do that. It’s understanding the personas, and competencies of the founders, seeing where your weaknesses are, and what adds the most enterprise value in the most logical and prioritized way. That’s how I think about people.

I’m switching the topic here a bit. Let’s discuss being a mentor. There’s a famous quote, “A great person needs to have a mentor and a protégé simultaneously.” Do you mentor others? Do you have a mentor?

Wealth Building Strategies: We break into three personas of people in the company: the builder, the seller, the measurer.

Not only do I believe in what you said. We have gone to the level of starting a not-for-profit that focuses on the art and craft of mentoring and mentee-ing, so being an effective mentor and mentee. We have found in the world that there have been a lot of mistakes made that set people back as opposed to advancing them forward, which is what the point of mentorship is.

I could go for hours on how important it is for a person to seek out mentors and coaches to make less mistakes than the ones who went before them. You hear the terms about standing on the shoulders of those who went before you. There are countless numbers of people that want to mentor, and they want to take the knowledge and help people draw insights out of their future and so on. It’s an endless topic. One hundred percent, I support it. I mentor super actively across tons of tech accelerators across our portfolio, founders, and so on.

In the act of mentoring, I say to people that having a protégé makes you a better human and leader and makes you think a little bit differently about how you interact. It makes you a better person. I have found that personally. It’s shaped me differently since I’ve actively started to pursue this. Yes, on both sides. I believe in mentoring. I am always learning.

For those who are continuous learning or growth people, you want to have mentors. By the way, mentors can be peers. They can be subordinates in the corporate hierarchy. They can be younger people who are working on crypto and blockchain every day of their lives that I want to become educated on. It is not what you think where the older person mentors. It can take all shapes and sizes as long as you’re open to it. That’s how I think about mentorship.

That question was strategically put into place so Ava could ask you if you would be her mentor.

I have to eat my own cooking. I commit to you guys that I will give you some time outside of here to mentor on some of your business building.

That’s super exciting to hear, Brice. That made my day. What is your advice to passive investors looking to start investing in real estate private equity?

To start investing in real estate, there are accredited and unaccredited. Let’s assume they’re accredited, so we at least get past that hurdle. The starting point for real estate investing is interesting because we all touch it usually by virtue of homeownership. If you’re accredited and thinking about investing in real estate, I’m going to make an assumption that you probably own a home.

You’re starting to accumulate a store of wealth. We can debate. A lot of people talk about your primary residence as not an investment. It’s a personal use situation. I do think it is, in a way, a store of wealth, which means there’s an investment concept to it, so you already have started likely. That’s usually private property.

There is value to public REIT investing plausibly to start your real estate journey. It gets you to learn about the sectors of real estate, and all the asset categories, like industrial, retail, residential, commercial, office, digital infrastructure, data center, towers, fiber, and so on. You start getting educated across the board.

You’re then deploying. You’ve got security selection and all that kind of stuff that’s going on. You’re learning. As you’re doing that, there is then a way to enhance, in my view, that whole process by seeking out private alternatives. We are very active investors in private places that we couldn’t get exposure to by virtue of the public REIT markets. Condo development is one example and there are a million others.

If I could go along the continuprimary residence, and get your house. You’re accredited. Two is the public side to understand the asset category and get some smaller amounts of play and a bit of diversification. Maybe an ETF or two if you want to go in the structured product world. You’re then going to find the holes.

Mentors can take all shapes and sizes as long as you’re open to it. Click To TweetWhere those holes are, you then start seeking out people like you or managers who’ve created a product that is available at whatever size, scale, or asset categories you want to diversify into. Build the trusted relationships, do your due diligence, and then start to deploy capital. That’s how we did it on our side.

We’ve asked the same question from people who are only focused on real estate private equity. Brice’s answer was more sophisticated than lots of other guests. No insult to our other guests. It’s the next segment of our show. Thank you for all that. I’m sure our readers gained a lot of golden nuggets and knowledge from that. Let’s start the rapid-fire.

The Ten Championship Rounds to Financial Freedom.

I’ll do my best here.

Whatever comes top of mind. Here’s the first question. Who was the most influential person in your life?

My grandfather, at the earliest age. He was a farmer in Saskatchewan. To this day, he has probably the most amazing work ethic. When we talk about talent, character, and integrity, the man had it in spades. Until the age of about twelve, I wanted to be a farmer. That’s how much I idolized him. Sadly, he has passed. He was a great man and a great influence on my life. I stand by him as my benchmark for the character, integrity, work ethic, and what he instilled in me.

Your family owned some farms in Saskatchewan.

We do.

Sadly, how it goes. Over time, the older generations retire and pass on. The next gens all started to become in the city and doing those kinds of jobs and so on. Eventually, it got sold. It was formative for me to grow up in Saskatchewan and to be exposed to a more middle-class setting like a farming culture. It was fundamental to who I am now.

I can relate. Next question, what is the number one book you would recommend?

Financial-literacy-focused?

Anything.

Even though the questions are financial-related, this is any book.

I’m going to give you two. I’m going to do one on financial literacy and one on mindset. I did a Finance degree at Dalhousie in Halifax. I graduated in 1994. In theory, I came out of university trained about what we’re talking about now. The reality is that the training was completely wrong for personal finance management and planning, which blows me away to this day.

When I tell you about this book, I do it with the caveat that this is a degreed individual. I’ve got a Bachelor of Commerce with Financial and Finance as my major. Even I needed to learn. The book is called The Psychology of Money by a gentleman named Morgan Housel. There’s also a free blog post that’s very lengthy and talks about what created the inspiration for the book. This book came out in 2020. It culminates in my entire view of financial literacy. The number one issue in investing is behavior.

Everything else can be taught, asset allocation, fees, security selection, and taxes, all that stuff. The number one issue is how you behave when the chips are down. Let’s use the example dot-com. I’m a young guy building my wealth. The NASDAQ drops by 80%. The S&P drops by 50%. What do you do the day after that? How do you react to that? The short on it is behavior. Housel wrote a book about this. Everyone should either read the book or read the blog post.

Antifragile: Things That Gain from Disorder

The second book that I recommend is on mindset. How do you understand that when things are stressors, when they’re negatives and crises, there are various ways one can react? The best way generally to react is in a way that seeks the opportunity within the crisis. The book that set the stage for this, there’s a lot about resilience in this book and so on, is called Antifragile: Things That Gain from Disorder. It’s written by a very famous author named Nassim Nicholas Taleb. I can’t recommend that book enough around creating a mindset and understanding of how to react better to stress and crisis.

Next question, Brice. If you had the opportunity to travel back in time, what advice would you give your younger self?

I did not understand the power of compounding. I would never want to relive my life. I’m blessed on all levels with a beautiful social, beautiful wife, and beautiful business building. I love everything about that. I actually would have told myself to get saving and compounding earlier. That is the most important thing that I missed as a youngster. Thankfully, I caught it up, but I would have started a lot earlier.

What’s the best investment you’ve ever made?

Various ways of measuring return, but the largest dollar investment return that we’ve had is the wireless company we started and sold a few years ago. It was called WIND Mobile. It is now called Freedom Mobile in Canada. That was what set us up with the liquidity to have our investment platform. By that measure of the size of dollar gain, that was the winner. There are other measures, like IRR, Multiples, and so on. It’s probably not the biggest, but it was the most impactful.

What’s the worst investment you’ve ever made, and what lesson did you learn from it?

There are two ways I would answer this question. One is I’ve invested in a bunch of micro-cap public stuff. That’s almost gone to zero. Why did I do it? I didn’t follow my own rules. The lesson is to follow your rules. I have a framework for investing and then I got a call from someone that I know, and they’re like, “You should buy this little stock here on a stock tip. Go buy this oil stock.” I go buy it, and it goes to zero.

I do no due diligence and I just take the tip. There’s a whole category of investing that’s that behavioral thing again, where even when you have rules, someone calls you, and you violate your own rules, never violate your rules. That’s point one. The second way I would answer this is I’ve taken zeros on the venture and tech investing I do when we come in very early.

The lesson there is very simple. You should expect to take zeros on those investments or else you’re not taking the right amount of risk in that asset category because portfolio construction in venture requires a risk profile where some breakout huge and some go to zero. I am okay with those zeros because it was part of a process.

How much would you need in the bank to retire now? What’s your number?

If I want to meet my definition of freedom and control of time, burns rate covered with passive income, I’m past that number. For me, it’s not a huge number because I live a reasonable lifestyle, so I don’t need $100 million or anything like that. Here’s what I would say to you. Whatever the definition of freedom and control of your time, you have to do things that drive you to get you up in the morning every day, keep you motivated, inspired, charging forward, learning, and growing. For me, it was very interesting. As we came out of the operating side and moved to the investing side, I actually found a holy passion. I love what I do every day.

When things are stressors, negatives, or crises, there are various ways one can react. The best way to react is in a way that seeks the opportunity within the crisis. Click To TweetI love meeting founders, mentoring, investing, and so on. Again, that will be cliché, but you don’t consider what you do at your job. It is very true for me. I keep doing this to keep the mind going, but what I have done is I’ve done a lot more impact-related work, which is a product of having more time. I’ve been able to do a few things that I wouldn’t have been able to do as a straight-up operating person. I’m at my number, and it’s much more now about making choices and what one wants to do to be smart, impacted, and learning as possible.

If you could have dinner with someone dead or alive, who would it be?

That’s a hard one because there are a lot of people in the category and it would be dead because I would need to understand some of the fundamental historical truths and untruths. I’ll pick one. Major religious figure. Let’s pick Jesus Christ, but it could be others. I would want to understand what reality was there, what it wasn’t, and get a flavor for that, but there are lots of people within those categories. You have this manufactured construct. As they say, history is written by the victors. I would want to try to go below the surface and understand these big seminal moments with someone who’s already passed, and there are many, but I’ll pick one for that.

If you weren’t doing what you’re doing, what would you be doing now?

At 50, I have met my number. I have the control to think of doing something else right now. The challenge for me is how do I keep myself engaged doing something different as inevitably will happen or want to slow down the work pace in what I’m doing day-to-day, as I’ve mentioned. It’s a bit of a challenge and something that all of us who run pretty hard in what we do every day, there’s a day where that slows. The question becomes, what does that look like the next day? For me, I don’t know the answer to that yet. Is it picking up something different?

Would I want to be a prof talking about entrepreneurship at a college? That’s not that far off from a lot of the mentorship that I do. I could imagine if I had done that. I get sucked right back into what I do every day. Do I want to sail off into the sunset, move to a warm destination, and pick up? I used to be in the Naval Reserve. Do I want to start sailing again and living that lifestyle? Candidly, I don’t know. It’s a very important question that I think about a lot right now as the next phases of life come closer and closer. Excellent question. I don’t have a great answer there.

This is my favorite question, book smart or street smart?

Street smart, for sure, but I will caveat it. I encourage those who are more street smart than book smart to start to understand the concept of getting a little bit more book smart by looking at frameworks on how you do things. I’m a huge fan of Charlie Munger, Warren Buffett’s business partner. You guys will know that name, of course. Munger has built this whole philosophical thinking around the use of mental models not to have to learn everything from scratch.

What I would say to the street smart person is, “Good on you. You’re lucky you’re street smart. You’ve got that basic, but you need to back into the thinking of some of the best minds around mental models, frameworks, playbooks, and so on to help you do things better, faster, stronger, and not make all the same mistakes that the person before you made,” so I do caveat it.

Where will be the great place to reach some of those mental models? Is it through books that Charlie has authored, or what would be it?

Charlie Munger: The Complete Investor (Columbia Business School Publishing)

There is a book on him written by a gentleman named Tren Griffin called Charlie Munger. I didn’t put this book out there for you guys, but it’s an excellent book, partly because it has chapters that are unrelated solely to investing. It talks about the psychology of human misjudgment and a bunch of other important things in terms of the mind.

There are a few books. I’d be happy to send a few to you if you post notes or anything like that, that talk about mental models, but I’ll give you a website. There is a group in Canada who are also Munger acolytes disciples called Farnam Street. Interestingly, Farnam Street is the street where the headquarters of Berkshire Hathaway is. The guy is a complete apostle of these guys.

He has created a business focused on taking what Munger talked about and turning it into business. He has written three books on mental models, and he also has this incredible website and podcasts that are all about learning from those who came before you to make you move faster, smarter, and stronger. Farnam Street, a website blog podcast, and these books they’ve written on mental models.

Last question, Brice. If you had $1 million cash and you had to make one investment now, what would it be?

We are very concerned about valuation, in general, across the board. We have seen what’s happened over 2020 and 2021 in almost all asset categories, particularly in North America. Here’s what I would say to you. We think about this every day because we have this challenge. I’m going to cut it in half and put half of it in a non-North American equity market, which has very large pockets of value that I think over the next twenty years will have a lot of forces in its favor. That market is China, and I would suggest that China A-share style of investment. On the Mainland, the Shanghai exchange type of investing. The reason I say that is twofold. Number one is China recalibrated itself over 2021 when its market got hit.

It took a lot of action against some very successful tech entrepreneurs and scared everyone. China does that every once in a while. That caused quite a downtick in the Chinese equity market and has created pockets of value. We know the power of China over the next twenty years will continue. I believe there’s an interesting entry point into the Chinese equity market.

Now, looking forward about 20 years, keep that long-term thinking. The second half is, I would probably put with a venture capital manager that I trust that has proven themselves time again to be ahead of the curve on thesis and trend. It gets me into the innovation economy and keeps me running with the smart intellectual capital advances that are going to happen. Those would be my two for right now.

It did more sophisticated than, “I would buy multifamily,” which also our guests would say. We really appreciate that, Brice.

Maybe you could quickly tell people what the best way that they can reach you is.

I’m on LinkedIn, so hit me on LinkedIn. The second way is I do a little bit of tweeting. Not that much, but feel free to follow on Twitter. The best way is definitely LinkedIn.

Brice, we really appreciate it. We’d love to have you on again at some point in the near future. I appreciate all the knowledge.

I’m looking forward to your mentorship. Thank you so much.

Thank you. I really enjoyed it and hope there’s some value there. I look forward to the next time.

—