If you want to succeed, you have to educate yourself. Do you want to get stuck in a job that’s draining you out? Or are you open to learning new opportunities that could help you grow and thrive? Tune in to this episode as Ava Benesocky and August Biniaz interview Chris Larsen on how you can use passive income to achieve financial independence. Real estate investors need to equip themselves with the proper knowledge and strategies. In this conversation, Chris dives deep into life insurance policies, private equity, cultivating relationships, partnering with investors, acquiring multi-family assets, and so much more!

Get in touch with Chris Larsen:

Email: jchris@nextlevelincome.com

LinkedIn: linkedin.com/in/nextlevelincome

Website: nextlevelincome.com

YouTube channel: https://www.youtube.com/channel/UC7ryurcdx6zl1wqpb0la2JA/videos

If you are interested in learning more about passively investing in multifamily and Build-to-Rent properties, click here to schedule a call with the CPI Capital Team or contact us at info@cpicapital.ca. If you like to Co-Syndicate and close on larger deal as a General Partner click here. You can read more about CPI Capital at https://www.cpicapital.ca. #avabenesocky #augustbiniaz #cpicapital

—

Watch the episode here

Listen to the podcast here

Important Links

- Next-Level Income

- Book Link – Next-Level Income

- Banking Link

- Blog – Next-Level Income

- Podcast – The Next-Level Income Show

- United Van Lines

- Lifespan

About Chris Larsen

Christopher Larsen is the founder and Principal of Next-Level Income. Since “retiring” after 18 years in the medical device industry he dedicates his time to helping others become financially independent through education and investment opportunities. Chris has been investing in and managing real estate for over 20 years. While completing his degree in Biomechanical Engineering and M.B.A. in Finance at Virginia Tech, he bought his first single-family rental at age 21.

Christopher Larsen is the founder and Principal of Next-Level Income. Since “retiring” after 18 years in the medical device industry he dedicates his time to helping others become financially independent through education and investment opportunities. Chris has been investing in and managing real estate for over 20 years. While completing his degree in Biomechanical Engineering and M.B.A. in Finance at Virginia Tech, he bought his first single-family rental at age 21.

Chris expanded into development, private-lending, buying distressed debt as well as commercial office, and ultimately syndicating commercial properties. He began syndicating deals in 2016 and has been actively involved in over $1B of real estate acquisitions. In addition to real estate, Chris owns multiple car wash locations across the Southeast. Chris lives with his wife and two boys (and Viszla, Lucy!) in Asheville, NC where he loves spending time with them in the outdoors and enjoying the food and culture that the region has to offer.

To Go From A Six-Figure Career To Six-Figures In Passive Income. Multifamily Investment – Chris Larsen

We have another great episode for you. Please like and subscribe as it helps us build our channel and allows us to keep bringing you great content and expert guest speakers. Our mission is to empower investors to earn passive income through real estate investing. We are joined by Chris Larsen. Chris is the Founder and Managing Partner of Next-Level Income. He has been investing and managing real estate for years.

While still a college student, he bought his first rental property at age 21. From there, Chris expanded into development, private lending, buying distress debt, as well as commercial offices. Ultimately, syndicating multifamily properties. He began syndicating deals back in 2016 and has been actively involved in over $400 million of real estate acquisitions.

Chris is passionate about helping investors become financially independent. August and I believe this interview with Chris will bring great value to anyone who wants to learn how life insurance could be a powerful tool in investing in real estate. This interview will also be helpful to passive investors looking to choose the right sponsor to partner with. Thank you so much for being here, Chris.

Welcome, Chris.

I’m excited. I’m married to a Canadian so one of my favorite things to do is cross borders here. This is a real treat.

We’re excited to have you on. If you could please start by telling us about your background and your start in real estate, please.

Thank you for the introduction. I’ve been doing this for more than half of my life. At 21, I bought my first property in college. You mentioned the life insurance piece, which we’ll go back and touch on that. In my book, I rewrote and added chapter three called Your Opportunity Fund. It’s all about how we use life insurance to maximize our real estate.

If you’re reading this, you can get a free copy at NextLevelIncome.com. Click on the book link. You can download it or I’ll even send you a copy if you put your address in there. I went to school for Engineering. I knew two weeks into my freshman year that I didn’t want to be an engineer but it was okay because I was there to race my bike. I wanted to be a professional cyclist. I started to race when I was fourteen and built my days around my cycling.

It was formative because as a cyclist, you don’t make a lot of money. I was always looking for other ways to make money. I learned that you could move time around in the day to have the freedom you wanted to do the things that you wanted to do and college is great for that. You have a lot of freedom that you don’t have in a lot of areas of life. In between my freshman and sophomore years, my best friend, my training partner and roommate in college, Chris passed away. He had a massive brain hemorrhage.

I went back to school and raced for another year. I was an All-American Cyclist that year, the state champ. I won a lot of races and wasn’t happy. I came back to school. I quit cycling and racing. Here I am in my junior year of college. I didn’t want to be an engineer. I’m not racing my bike. My team went pro and I quit. I lost my friend network and did not enjoy school. I was depressed.

One day it dawned on me like, “I need to make the most out of every day. I can’t live with regrets anymore.” I’ve got to honor the life that I have and the life that Chris doesn’t have. You have to have money to be able to have freedom. I was always entrepreneurial. In that year, I started day trading the stock market because I had to fill this void of 15, 20 and 30 hours a week where I used to ride my bike.

At some point in your life, you realize that you need to make the most out of every day. You can’t live with regrets anymore. Click To TweetI have all this time, extra energy and brain capacity. I was still going to the gym. I devoured book after book on finances and read online on the stock market and everything I could learn. I read 250 books. As I started day trading, I was making about $5,000 a month as a junior in college. I was not happy again. I’m here laying at 3:00 AM thinking, “Do I want to do this for the rest of my life?”

I kept searching for other areas of investment. That’s where I came upon real estate and how I bought that first property. It was a townhouse. It was for sale right up the road for me. I bought it and moved in. It was a house hack. I rented out the other couple of rooms. I bought the place next door and rented out those three rooms. I had my 1st mini 6-unit multifamily property where I rented 5 of the 6 rooms out. I moved and started from there.

You were still in college at this time?

I was a junior, maybe senior. I bought that second property in college. I decided I’m going to be a real estate investor. That was the initial start of that whole process.

You were making money day trading with stocks so then you were able to buy real estate with that while you were in college.

I had $3,000. That’s what it took me to buy that first property. I had my mom co-sign. You don’t need a lot of money to get started in real estate.

Unless you’re from Vancouver or Toronto, then you need $1.3 million to buy a property.

You need to move and then you don’t need a lot.

I want to discuss your background in Engineering. You knew it right away but it’s a numbers and data-reliant industry. You need to be extremely diligent and fastidious to be an engineer. Maybe talk to us about how getting started in that was beneficial to you as a real estate investor.

It’s funny because I would go interview and people would be like, “Chris, you have an Engineering degree and MBA in Finance. You want to sell pharmaceuticals.” I ended up in the med device and people were like, “What are you doing?” I didn’t want to be an engineer. I knew that. I always joke. My counselor pulled me aside and said, “Chris, you’re not smart enough to be an engineer. You have too much personality. You should look at something else like sales,” which is what I ended up doing.

The cool thing is you learn a thought process as an engineer. You learn to make assumptions, question those assumptions and a systematized way to solve a problem. I learned this way of thinking over these four years because every day I’d go home after classes, go through this process and solve problem after problem. I had learned to program and I did not enjoy it but it got ingrained in my brain.

Passive Income: The cool thing is you learn a thought process as an engineer, and you learn to make assumptions.

What is awesome is it’s the same process you have to go through when you’re analyzing a property. You look at the assumptions, the data and the numbers. You then say, “Can we follow the same systematized process to get a specific outcome within a range? Can you repeat it?” Engineers will say the word iterate.

What iterate means is you try something, improve on it and do it again. That process got ingrained in my brain. Even the fact that I never was a true engineer, I passed the PE, the Professional Engineering exam. A lot of people say, “You are an engineer, Chris.” I never practiced but I still use that process every single time I look at a deal.

Passive Income: Iterate means you try something, you improve on it, and you do it again.

Unlike law and other practices, you can negotiate. It’s a numbers game and math.

Repetition developed his mind to be good and he utilized that.

You can challenge and analyze the data. You can look at different things in the data but the data is the data. It is what it is.

You can challenge and analyze the data. You can look at different things in the data, but the data is the data. It is what it is. Click To TweetIt’s like underwriting multifamily deals where emotion is part of it but it goes by those data. Their offers come and all these other metrics in the business.

Doing a bit of research on your background, we could see you’ve been involved in investing in multi-asset classes and property types within the real estate asset class itself. I have a question for you. What was it in particular about multifamily for you to have labeled it, “The holy grail of real estate investing?” I believe you started as a passive investor initially. If you could touch on that as well, please. That would be helpful.

The subtitle of my book is Using the ‘Holy Grail of Real Estate’. I became a medical device sales rep. It’s an amazing field. I got to work with these amazing technologies and geniuses like orthopedic surgeons orthopedic spine surgeons, neurosurgeons and brain surgeons. I got to work in the OR with these individuals and be on a team as they did the surgery. It was a cool, rewarding and also very arduous career where I worked 7 months straight, 1 time without a day off. I spent three days straight, nights included in a hospital while I was working on call. I’d work 40, 60, 80, to 100-hour weeks. I worked a lot. It was financially rewarding but it wears you out.

A regular job can be financially rewarding, but it can wear you out. Click To TweetAt the time, I was also managing that portfolio that I built, which is single-family property. I was in my early 30s to my mid-30s. I have two young boys at this point and I’m like, “The last thing I want to do is take a phone call from a tenant on my honeymoon dealing with the problem.” It wore me down. I got introduced to multifamily in a meeting with my wife. I looked into it and it started to check all the boxes.

I’m a data guy so I looked at the demographics, the ability to control or force appreciation and the fact that you had income, appreciation and depreciation. When I looked at the risk-adjusted return on multifamily, it had the best risk-adjusted return of any asset class. I felt that this was going to persist for another 1 to 2 decades, which were right in the middle of those 2 decades. Look at how strong it still is. It has such demand.

When you added all that up and the ability for me to be a passive investor and make better returns than I was making managing my single-family, I was like, “This is a no-brainer and the holy grail.” I felt like I found the holy grail. I started as an investor and did that for a few years. I had conversations with friends. They were like, “I’d love to be involved.”

My first partner and I analyzed this and talked. He was an engineer as well or was trained like I was. We were like, “We have as much or more experience in real estate as the group we’re investing with.” We partnered with them, bought our first deal and that’s the deal we closed in 2016. We’re in many years now with active syndicators.

I want to touch on some of those points that you talked about to why multifamily is the holy grail in your quote on investing but briefly go over it. You got the cashflow component, the natural market appreciation which multifamily happens to appreciate better because it’s such a sought-after asset class. You got force appreciation. It is going in and adding some form of value add to force appreciation of the asset. You then got depreciation that you can utilize over tax purposes. It hits not only two main fundamentals of real estate investing, which is cashflow and natural market appreciation but it’s also got force appreciation and tax benefits. I agree with you.

My MBA is in Portfolio Management and there’s a ratio we call the sharp ratio. That’s a risk-adjusted return. If you haven’t heard of this before, the sharp ratio sounds fancy and it is fancy, it’s a calculation but it’s how much of a return you get based upon the risk that you get out there. There’s something called variance drag but my point is, you’re going to get a better overall return in an asset that has an average say 10% to 20% range of returns.

Let’s multifamily gives between 10% and 20% range of returns so the average return is 15% versus the stock market. I’m simplifying, trying to be very positive here. Let’s say the stock market average is between 0% and 30%. That has negative returns but you’re going to do better over time with that asset class that has steadier returns. Especially when the market drops and it has negative returns, you’re going to have a real drag on that portfolio.

I always ask this question, “The stock market has an average return of 10%.” “Yes, but you want to know the compounded annual geometric return? That’s what you get.” If you’re reading this, you’re like, “What are you talking about?” That is the actual return, not the average return. It’s called the CAGR, Compounded Annual Geometric Return.

It’s very simple. Let’s say, you have $100,000 in the stock market and it drops 50% and goes up 50%. They’d say, “Your average return is zero. You should have zero.” You lost 25%. You went from $100,000 down to $50,000 and back up to $75,000 so you’re down 25%, even though your average return was 0. That is why I like to be in asset classes that have a much higher sharp ratio and less volatility. You’re going to do better over a lifetime of investing, even if the “average return” is the same. It’s like free returns.

The stock markets view themselves as these returns that they’ve provided over the years. They don’t count the drops and the rises. They mention these returns as 6% and 8% but when you do go look at it in more detail, you realize, “That is not the case. It is much lower than that.”

Let’s discuss syndication or as we like to call it here, real estate and private equity. Talk to us about your start in private equity and your journey of cultivating relationships and then partnering with investors to acquire multifamily assets.

I went from a passive investor to partnering with the group that we worked with to do our first 100-unit deal, which was in the Atlanta market. Word spread and people were like, “What do you do? How are you doing this?” When I left my W-2 role, it exploded.

When you say the group you worked with, you’re talking about the operational part of the component, not the group of investors?

When I first started, it was myself and one other partner. We did everything like acquisitions, management, investor relations, capital raises and underwriting. He ended up taking on more of the operation side of things because I was still working the “9:00 to 5:00 job.” Although I worked about 16 hours a day, 6 days a week to manage both my business and my med device career that I was still working on. We were investing with a syndicating group. We partnered up with them to do our first deal. They were consultants on that first deal.

My partner and I did 5 deals together over the next 3 years. We bought five different communities in the Atlanta market. This was years ago. A lot happened over the last couple of years. We started to expand into other markets in the Southeast so North Carolina, South Carolina, Florida and Texas. The group I work with has expanded. I’ve started to move more into my lane. I still do the underwriting side of things looking into deals but I’ve started more to handle the investor relations side of things. As it’s grown, we have over 500 investors. You can’t do everything but you can when you’re doing 1 deal a year and there are 2 of you.

Maybe we can touch on the next subject here, the relationship between the general partner and the limited partners, the investors that trust in you to then make the investments or bring this whole team together to look at the deal that’s being presented by your operating partners, presented the project to your investors. They see you as the steward of their investment. It’s a very important relationship as people are investing with you their hard-earned money.

I want to touch on another concept to where we’re being somewhat introduced which is utilizing life insurance to be able to then make real estate investments on the passive side or the active side. Talk to us about how this works. What is this concept? Some people reading, when they did this the first time, were like, “What are you talking about life insurance? When I go to the bank and they try to push me on this life insurance thing, I always say, ‘No, thanks,’ and I leave. You’re talking about life insurance and then utilizing it to invest in real estate. What are you talking about?”

What Chris is about to share with us is a very powerful concept that we’re falling in love with and we can’t wait to share it with our network.

It’s the rich and top 1% use and then it’s being available to everyday people.

I put my money where my mouth is. I am doing these strategies and investing my money. For every deal we do, I’m in the process of starting 2 new policies that are 5 times what our previous policies were with my wife and me. I believe in this. I also have a very personal relationship with life insurance. I worked for State Farm years ago, I was a licensed agent back then. I sold life insurance.

I learned by term invest the difference. Life insurance isn’t a great investment. That’s what I heard and told but here’s what I found out. The richest families, the families that are worth a lot of money, the Rockefellers that have perpetual wealth, that has money that goes from generation to generation, are using strategies like multifamily, commercial real estate investing and whole life insurance.

If you’re thinking, “I’m tuning out. Chris mentioned whole life insurance.” First off, I don’t want you to think of it as an investment and here’s why. My father died when I was five years old and he had life insurance. That life insurance allowed my sister and me to go to college and come out without any debt partially because of the money he left, which wasn’t a ton but it was enough combined with me working and scholarships to get through school without any debt. That’s the first thing.

The second thing is people are like, “Chris, I can get a better return on my money by investing elsewhere.” My best friend asked me what I did for insurance. He goes out and gets policies on himself and his wife. Three years later, she passes away from cancer. He tells me, “Chris, I can’t thank you enough. I ended up getting policies for my wife.” I was stunned because I didn’t know he did that. He just asked me what I did and went and did it.

What was his return on his investment? Do you want to ask somebody who lost their wife that question? Do you think he thinks about it that way? Life insurance is not an investment. It is a tool. After I heard that story from my friend, I put this chapter in my book during COVID. I got relicensed because I’m like, “This is something that I need to teach people and be able to understand at a higher level.” If you blend it with the strategies with syndication, it is so powerful.

Life insurance is not an investment. It is a tool. Click To TweetFirst off, go to our page, NextLevelIncome.com. There’s a banking link. We have a white paper and a little webinar on there where you can see how this goes into play. If you’re into real estate, here’s how you can think about life insurance. Term insurance is like renting. If you’ve ever rented, you rent and pay a set amount of money for a year, a couple of years or whatever it is and then your rent goes up. How much equity do you have after your lease is over? It’s zero.

Term insurance is the same. On the surface, it seems like it’s cheaper to rent than to own and it is. It’s 30% more expensive to own a home than to rent in the United States on average. It’s cheaper to rent but you don’t build equity. Whole life insurance is like owning or a mortgage. You have a set amount of time, 7 years, 10 years, 30 years or 50 years that you pay a level premium and a certain amount but the cool thing with whole life insurance is it’s higher initially than term.

It’s like renting versus owning. It ends up being less the longer you get into your life. As you get older in life, it doesn’t make financial sense to get your whole life anymore because the insurance companies know you’re about to die. They’re going to charge you a lot more because it’s numbered. I’m an engineer and it makes sense to me this is numbers but with a whole life policy, you get equity. We have hundreds of thousands of dollars of equity in our policies after more than a decade of investing. That’s money we can access.

What my partners and I teach and put policies together for is we structure life insurance policies so they grow the cash value or the equity at a very rapid rate that accelerates the cash value portion. It minimizes the cost of insurance. This is why when you go to the bank or your financial advisor, they say, “You need a $1 million policy. We’re going to sell you a $1 million policy. You might have some cash value.” What we do is we say, “How much cash value do you want? We’re going to construct the policy to maximize the cash value. You’re going to get this great insurance benefit behind it.”

It dawned on me when I went to our attorney years ago. We were going through our process and he brought up my net worth. I was like, “That’s two times what I thought it was.” He said, “Right here, you have this life insurance policy.” He included that in our family’s net worth. I thought, “I doubled my family’s net worth by buying this permanent life insurance policy. This is what my attorney who’s planning for our future thought.” If you want to protect your family and increase your family’s legacy and net worth, permanent whole life insurance will do that.

If you also want to have something that can act as your bank, that can earn real rates of return, 4%, 5%, 6% that you can also borrow against, we teach strategies to borrow against using lines of credit secured by life insurance at rates of 3% to 4%, very low rates that you can then invest at 6%, 7%, 10% or 15%. Think about that. If you’re borrowing at 3% investing at 15% and you’re not having to touch your money in your policies, you have two pots of money growing at the same time.

There’s a cost to it. You’re paying for the insurance on the front end but it takes about 5, maybe 7 years at the most to break even and pay for that insurance. After that 5 to 7-year period, it’s 100% upside. It’s like starting a business in that sense or buying a house. When you get through that initial period, it’s a little more expensive than your equity grows. You’re way better off than if you were renting.

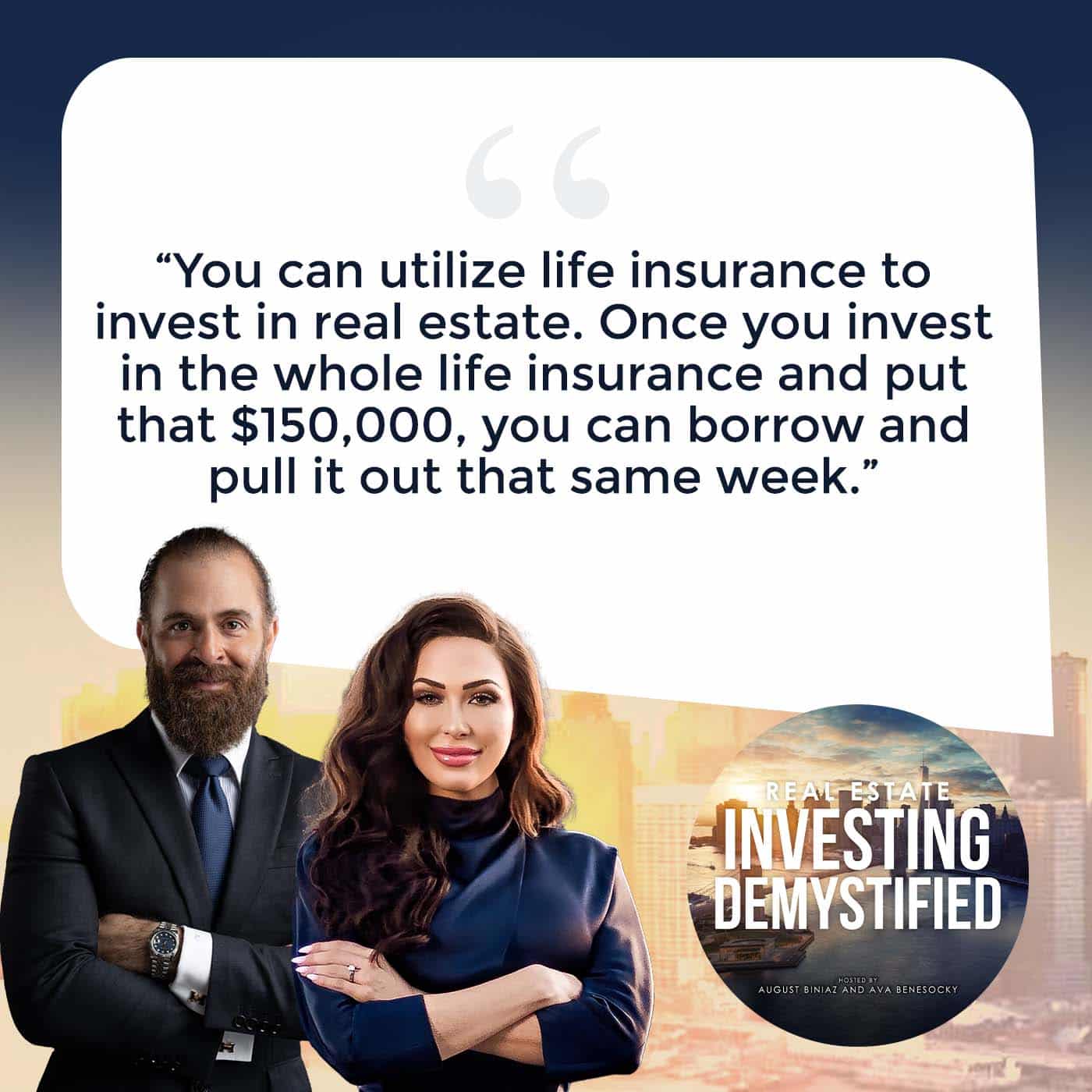

Let’s simplify it a bit. It’s the first time they’ve encountered it. Let’s use a case study of an investor who approaches your group or our group and says, “I got $100,000. I want to invest with your group.” We say, “Hold on a second. There is a way that you could use life insurance to be able to then invest with us.” If they go and buy a life insurance policy for $130,000 or X amount of dollars where it’s somewhat reasonable, depending on who they go to for the policy, they can borrow against that policy, the $100,000 that we’re going to invest with us.

They’re going to invest that $100,000 with us. The average multifamily passive investing gets 15% and they’re earning 15% on that investment amount but even though the line of credit was pulled against it, the policy in itself is still earning from that initial investment they’ve made. It’s risk leverage that they’re using to arbitrage.

The thing that blew my mind was once you invest in the whole life insurance and you put that $150,000, you can borrow and pull it out that same week.

A lot of times people get concerned, “If I buy this policy, do I have to keep adding to it?” That’s another incredible thing about life insurance. You can just buy that particular policy, even though it does make sense to keep adding to it. Even if you don’t, that gives you that leverage.

You’re double dipping your money.

I could tell you’ve seen the light. It’s complicated. I’ve worked with my coaching clients and we talk through it. It took me a couple of times to hear it and say, “Wait a minute.” Once you get it, you’re like, “Okay, it’s numbers.” Let’s use your example, August. I’m going to use round numbers. You may say, “I could do way more than that or that’s way too much for me.”

Let’s say you’re an investor. This isn’t uncommon. “I’m going to invest $100,000 a year for the next 10 years.” That was me. That was my plan years ago. I was making good money, a few hundred thousand dollars a year. We were doing development projects. My wife was working. We had the ability to do this. When you first start the policy, there’s that startup cost but if you put $100,000 in the 1st year, you’re probably going to have access to $75,000 to 80,000 of those immediately if you’re a young, healthy individual.

That $20,000 to $25,000 or 20% to 25% is going to go towards the administrative expenses, the upfront cost of the policy and the insurance. You’re going to start growing the policy inside that. After a couple of years, whatever you put in, if you’re putting in $100,000, you’re going to get even more than that back in cash value is what it’s called. I mentioned the 5 to 7-year period. Let’s say you put $500,000 in or $600,000, over 6 years or 7, at that point, you’re going to have more than that plus the return because you’re going to have to chip away at that initial amount you put in.

You’ve pulled out $75,000 every year?

No. Here’s the thing. You can pull out more than that after year one. It’s going to go close to $100,000 very rapidly. In only a few years, you can do that. If you say, “I want to invest $100,000.” If you put it through your policy first, why would you do that? Let’s answer that question. If you say, “We’re married and have a family,” that’s a great example of somebody that needs life insurance. They want to provide that security for their family. “I want to have this policy.” You start the policy. If you want to invest $100,000, you’re probably going to have to start with a little bit more than that but you put that money in, borrow it out and then you’re freaking out.

You’re saying, “I had $100,000 cash. Now, I have a loan for $100,000?” Think like a business person. You have a liability, which is on your balance sheet. You’re borrowing it at 4%. You have an asset that you’ve purchased a $100,000 investment in a real estate syndication. Let’s say you’re making 10%. You borrow 4% and earn 10%. You’re getting a 6% real rate of return but there’s something else. That $100,000 you put into your policy is untouched. It’s still growing because that loan is using life insurance as collateral. Your $100,000 is growing like my guaranteed rate of return or my rate of return on my policy is 5.25%. It’s growing at over 5%, which is even more than the 4% that I borrowed. It compounds.

I take the $10,000 from my $100,000 investment. I use $4,000 of it to pay the interest. I still have $6,000 left over. I put that into my insurance policy for the next year to start with that. You’re may be saying, “I’m locked into this. I have to do this.” Our policies set the pay period for about seven years. For somebody that says, “I’m going to invest for the next ten years,” you don’t have to do that. If you say, “I want to invest $100,000 and run it through my life insurance policy,” you have a minimum amount. You can set the minimum amount at $10,000 or $20,000 a year and then the max at $100,000. You have that range.

The thing is you never have to pay the loans back because it’s secured by your life insurance policy. You should pay the interest but you have the flexibility of when you pay them back and then the flexibility of how much you make on premium payment. It sounds great. It’s like, “I grew my money in two places. I’m comfortable with the cost of insurance. What’s the downside?” If you read this show, you probably understand real estate well. When you buy a house, you have a mortgage. If you have a lease, your lease ends in a year. You can move, switch places or move in with your parents.

Passive Income: You never have to pay the loans back because it’s secured by your life insurance policy. You should pay the interest, but you have the flexibility of when you pay them back.

If you have a life insurance policy and you’re like, “I can’t afford to make a $10,000 premium payment every year on a policy,” you shouldn’t start that policy. If you say, “I have $100,000 of excess cash. I’m comfortable having a policy that I can put that into. I have a business. I’m a physician. I’m a high-income W-2 earner. I have some stock options that are besting and I want to put those into something secure and going to be there for the rest of my life.”

If you have that consistent stream that’s coming in and predictable over the next years, you’re probably a good candidate to look at something like this. If you’re single and you don’t have a family, don’t have a high income or very unpredictable income that you’re not comfortable with something like that, maybe it’s not a good fit for you.

What if somebody lost their job and couldn’t make that premium that year?

What happens is there are options. You can do a paid-up policy. You can stop and pay up. Your total insurance is going to come down but there are options for that. You can even take policy loans to pay your premiums. If you’re like, “I can’t pay them for 1 year or 2,” you can take a policy loan. There’s a lot of flexibility. If you’re working with an agent that puts you in a policy that you can’t afford, that’s not a good agent. The salesperson who, “sales ice to Eskimos,” is not good. Somebody should tailor the policy to fit your situation and educate you so you don’t get into this situation that you’re in over your head.

Passive Income: You want somebody to tailor the policy to fit your situation and educate you.

One more thing, I wanted to share with people and correct me if I’m wrong but these big companies never lost money for people. They’re old and have never lost money for their investors.

We haven’t even gotten into why the life insurance industry is, in my opinion, so much more stable and great. Life insurance has been around longer than the IRS and the stock market. It’s been around a long time. The thing is these are numbers. I love numbers. If you say, “How do they pay this 4% or 5% rate of return?” If you have a policy with a mutual insurance company, the dividend is classified as a return on the premium. You don’t pay tax on that because if an insurance company collects $100, their expenses are maybe $92, $93 or $94. They have to collect more and make more with their investments than they spend.

Life insurance has been around longer than the IRS or the stock market. Click To TweetIf you’re a business owner, you’re like, “Chris, that’s called a business.” You have to make more than you spend. They have to do that and plan for this. They hire and pay actuaries. These are people that study the numbers for hundreds of thousands of dollars a year to do this. They’re the smartest people out there looking at these numbers.

What happens is at the end of the year, they have 4%, 5% or 6% leftover of that $100. That’s what goes back to their policyholders because they’ve spent less than they’ve collected and earned and done that. That’s why it’s so great. These companies have been around through the Great Depression and the Great Recession. They invest in things like commercial real estate like big class A multifamily deals and commercial projects because these are the smartest people wanting the most stable assets out there.

Passive Income: The smartest people wanting the most stable assets out there invest in commercial real estate, multi-family deals, and commercial projects.

With that premium you speak of, is that only when you borrow against the policy or is there a premium charge no matter what?

You have a minimum premium payment and then a maximum premium payment that you make. If you take out a loan, you have your loan payment and interest. If you were paying it back, my algorithm for paying back is I pay my interest on my loan because I want to pay that down. I don’t want my interest to compound. We want our interest on our investments to compound, not on our loans to compound. I then make my premium payments because that’s going to increase my cash value in my policy.

If there’s anything left over, I’ll make my loan payment after that and start to pay my loan down so I have that cash store built up for the future. Once you understand the flow and how to set everything up, what we specialize in is working specifically with investors because my agent that I started with when he heard what I was doing was like, “That’s awesome, Chris. I wish all my clients did that. Why didn’t you teach me how to do this?” I said, “I’m going to teach people how to do this.”

What is a premium on $100,000? Somebody gets a $100,000 policy. Let’s say they pull out $80,000, go invest in multifamily and they’re getting paid 10%, that offsets the loan they’ve borrowed and gives them some surplus but that premium is what I don’t understand. You have to add a premium. Where does that come into play? What is that?

It depends. If you say, “I’m going to put $100,000 a year into a policy,” that would be potentially your premium. The face value or the amount of coverage that you get would be based upon that number that you put it on. That’s where it’s backwards when it comes to “regular insurance,” where you go in and say, “I want a $1 million policy. What is it going to cost me?”

We’re going to start with the premium that you say you can afford or want to do over a period to fund your investments. We’ll engineer the policies to do that for you. It’s going to depend specifically on your situation, your insurability and all that thing. That’s about as clear as I can get without getting into the weeds here.

It’s tailor-made to each person.

It is. That’s why we work with different insurers as well because different insurers are better for people in different situations.

Thanks for your time to explain that to everybody. That’s awesome. I’d like to talk about the fact that you’re an author and then your book, Next Level Income. How did this idea come about?

Next-Level Income: How to Make, Keep, and Grow Your Money Using the ‘Holy Grail of Real Estate’ to Achieve Financial Independence

This is how the whole website Next-Level Income started years ago. I love what you do and that you have this amazing show and you share all this knowledge with your audience. What happened was I had these investments and people coming to me. I’d start to get calls and emails where people say, “Chris, I can’t invest yet but I want to know what you do, how you got to the point where you are and how to make more money or to get where you are. How did you do it?”

I have a phone call and write an email every week or so. Every week turned into every other day and then it turned into every day. I was answering the same emails and phone calls. I cut and paste. My partner in the podcast initially said, “You should start a podcast.” I was like, “I don’t want to work.” I then thought, “I’m already repeating myself. Why don’t I start taking these concepts and curating them?”

I started a blog and podcast. I wrote the book. Right before COVID, I got the idea to rewrite the book and add chapter three talking about this cash value, life insurance. It morphed into tremendous growth of the website and the podcast. We’re on episode 80 with the podcast. We had a start but the whole genesis of the book, the podcast and the blog was to curate and educate the next generation of investors.

Going back to multifamily.

You have places in Georgia, Texas and Florida. What are the other regions that you’re in?

The North and South Carolina. I feel like I might be leaving something out in there.

Tell us what interested you about these regions if you don’t mind.

Also, how do you go about choosing the region? Does it come with the region first and the possible operating partners within those regions? Does it start with operating partners and seeing what regions they’re investing in?

If you’re reading as an investor, that is the first question you should ask. I’m a demographic guy and I talk about in my book how I got into the med device because of the demographics, the Baby Boomers, are wearing their joints out and needed surgery. I talk about how my wife and I moved from the DC area to the Carolinas because of the demographics. People were moving here. One of the top growing states in the country is North Carolina. It’s been growing very rapidly for the past several years. It’s been a while since we moved here.

We moved to where we wanted to live, work and invest. You want to live with a rising tide. We live in Asheville, which we love. You guys are real lifestyle enthusiasts. You can make it happen. If you’re reading this, you can live where you want or where you vacation. We live in the Carolinas because we thought it was a good place to own real estate. The next thing we’re going to do is look around here for real estate.

Here’s a shortcut, especially if you’re in the United States. There’s a company called United Van Lines. Every year, they tell you where people are moving from and to. If you want to know where you should focus on your investments, look at where the moving vans are going. This probably isn’t going to be a secret.

They’re going to Texas, places like Denver, Colorado and some places in Idaho. They’re going to the Carolinas, Raleigh, Charlotte, Greenville, Charleston, Orlando, Tampa, the rest of Florida, Atlanta, Houston, Dallas and Austin. Does any of these cities sound familiar? This is probably where some of your friends are moving. That’s where you want to invest. You want to say, “I want to invest in these areas. What area do I want to invest in? Is it multifamily, industrial, commercial office or residential? What is it?”

You find operators in that area and find out who is best in class. Interview operators and figure out how they do things. Does it match up with what you think? Do they have a track record? Do they have a real team? Is it like a solo person that’s out there that if they get run over by a car one day, you’re out of luck because your distribution stopped and you’re like, “Where’s my operator?” You want to invest in a robust, knowledgeable team that has a great track record. That’s the process.

Once you figured out the geography, the sector and the operator, then you start looking at deals. Too many times, I had one of my coaching clients email me a deal. “What do you think of these deals? Do you know this operator? Why do you want to invest in these areas?” These are all the questions that I asked, “Is this the sector of the market that you want to be in?” Let’s back up a little bit, slow down and then we’ll start to look and see if this is a good deal that you should consider investing in.

Once you figure out the geography, sector, and operator, start looking at deals too many times. Click To TweetChris, what advice would you give someone looking to start passively investing in real estate?

First off, if you’re reading this, you have come to a great place. Educate yourself. Think about, “I read this episode. Does this make sense to me?” Don’t trust me. “Is what he’s telling me true? Is what Ava and August telling me made sense to me?” Go test it, look at it, talk to operators and start looking at deals like you’re going to invest.

If anybody out there has traded in the stock market and you can have a Phantom account where you Phantom trade and see what it’s like, look at deals. See how the operators treat you. Even if you don’t invest, see how they respond to you. See if you can look at the track record and the history of those deals. Talk to some other investors and get some other investors that have invested and have experience. Once you’re comfortable and you feel good, you’re going to have to jump in at some point but that’s what I would do for my next steps.

Here’s the next segment of our show.

The Ten Championship Rounds to Financial Freedom. Whatever comes top of mind, Chris. Here we go. First question, who was the most influential person in your life?

It’s my friend, Chris, who lost his life. My father passed away when I was younger so the period that I had with Chris and then the value that the experience of losing him provided in changing my mindset was the most influential.

What is the number one book you’d recommend?

I’m not counting my book and this is not a financial book. There’s a great book when I listened to a podcast with David Sinclair and Joe Rogan. It’s called Lifespan. You can have all the money in the world but if you don’t have health and life, then what good is it? Read Lifespan so you can learn some cool tricks to not only improve the longevity of your life but the health that you have during it and the quality of life that you’re living.

If you had to travel back in time, what advice would you give your younger self?

I use this on my podcast. I can’t wait to have you guys on and ask you the same question. Find a mentor earlier. Invest in that. I spend tens of thousands of dollars a year on coaching. I would go back and would’ve done that a lot sooner.

What’s the best investment you’ve ever made?

That’d be coaching.

What’s the worst investment you’ve ever made?

The worst investment would be the amount of time I spent with people that have a scarcity mindset. If you’re struggling and the people around you don’t support what you’re doing, you’re like, “What’s going on here,” you need to be around people with an abundance mindset. Don’t spend time with people that don’t have that.

How much would you need in the bank to retire now? What’s your number?

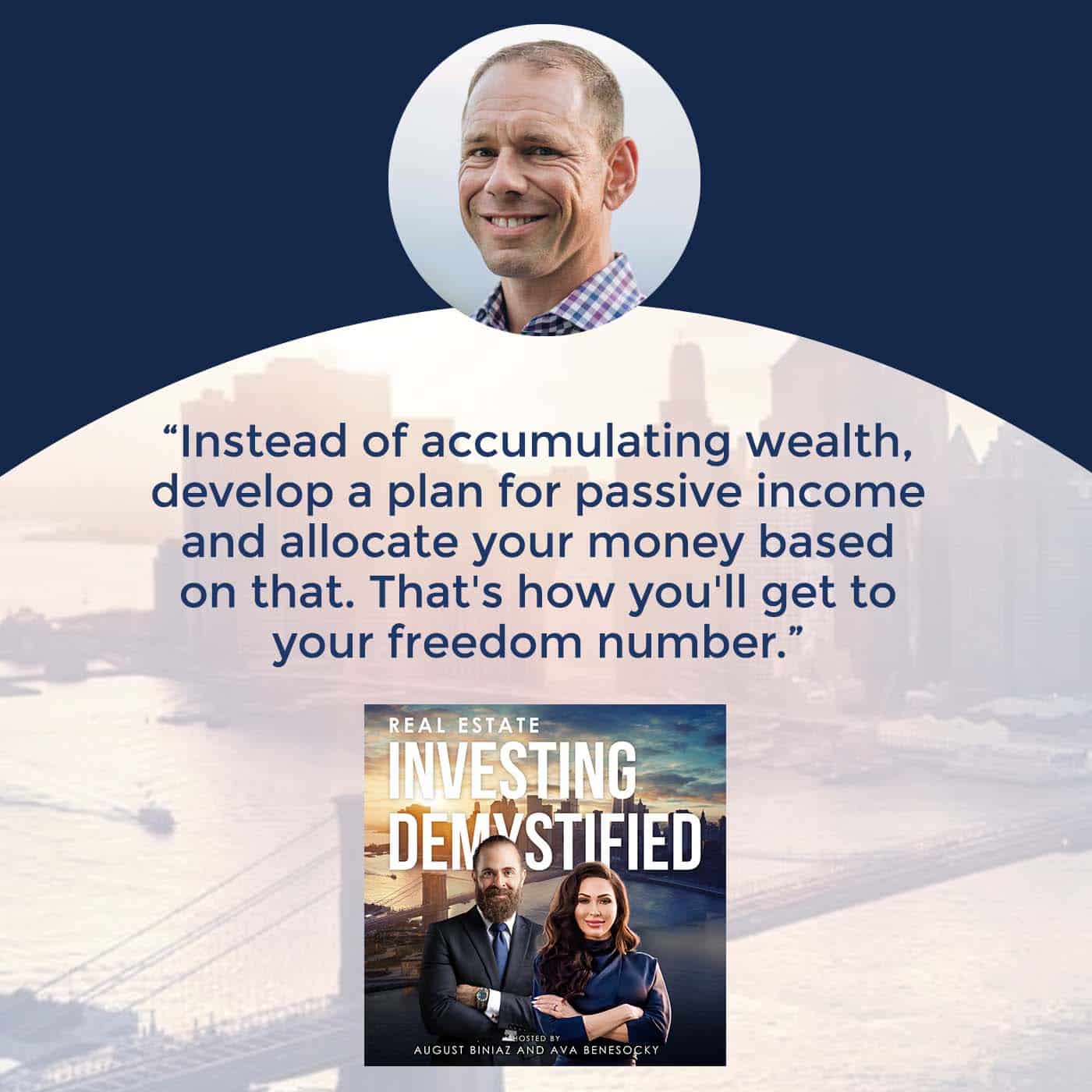

I got it but it’s simple. You need more passive income every month than you have in monthly expenses. You don’t need a massive net worth to make that happen. My philosophy is instead of accumulating a bunch of wealth and then saying, “I can spend 3% or 4% of this,” develop a plan for passive income and allocate your money based on that. If you say, “I need $10,000 a month to spend,” reverse engineer that. Figure out what you need to invest in at a specific rate of investment. That’s how you’ll get to your freedom number.

If you could have dinner with someone dead or alive, who would it be?

It’s my father.

If you weren’t doing what you’re doing now, what would you be doing now?

I’m very fortunate that I get to pick everything that I do but I chose a lifestyle route. I wanted a family, to have a full life, race and ride my bike and live in a beautiful area but if I went and listened to the devil on my other shoulder, I would’ve moved to Wall Street and been a Wall Street trader. That’s something that would be an amazing lifestyle to live. It’s a lot of pressure and that would be awesome to experience something like that.

This is my favorite question. Book smarts or street smarts?

You can either read more books or pay people. Henry Ford said, “I have a button on my desk to find the person that has the answer to that question.” You can pay people with the right answers. You can’t pay people to teach you street smarts so I’m going to go with street smarts.

Last question, if you had $1 million cash and you had to make one investment now, what would it be?

I’d probably spend it on experiences like travel with the family. I would probably invest it frankly but I would take a huge chunk of that and say, “We’re going to Italy for two months,” which is in our incoming plans here. You can take experiences with you. We’re big on experiences. We love that.

Thank you so much for taking the time. You have a very busy schedule. We love what you’re doing and your book. We’re sure that this added a lot of value to our readers.

Thank you so much, Chris.

You guys are awesome. I love your energy. I wish you wonderful holidays here with all the fortune in the world.