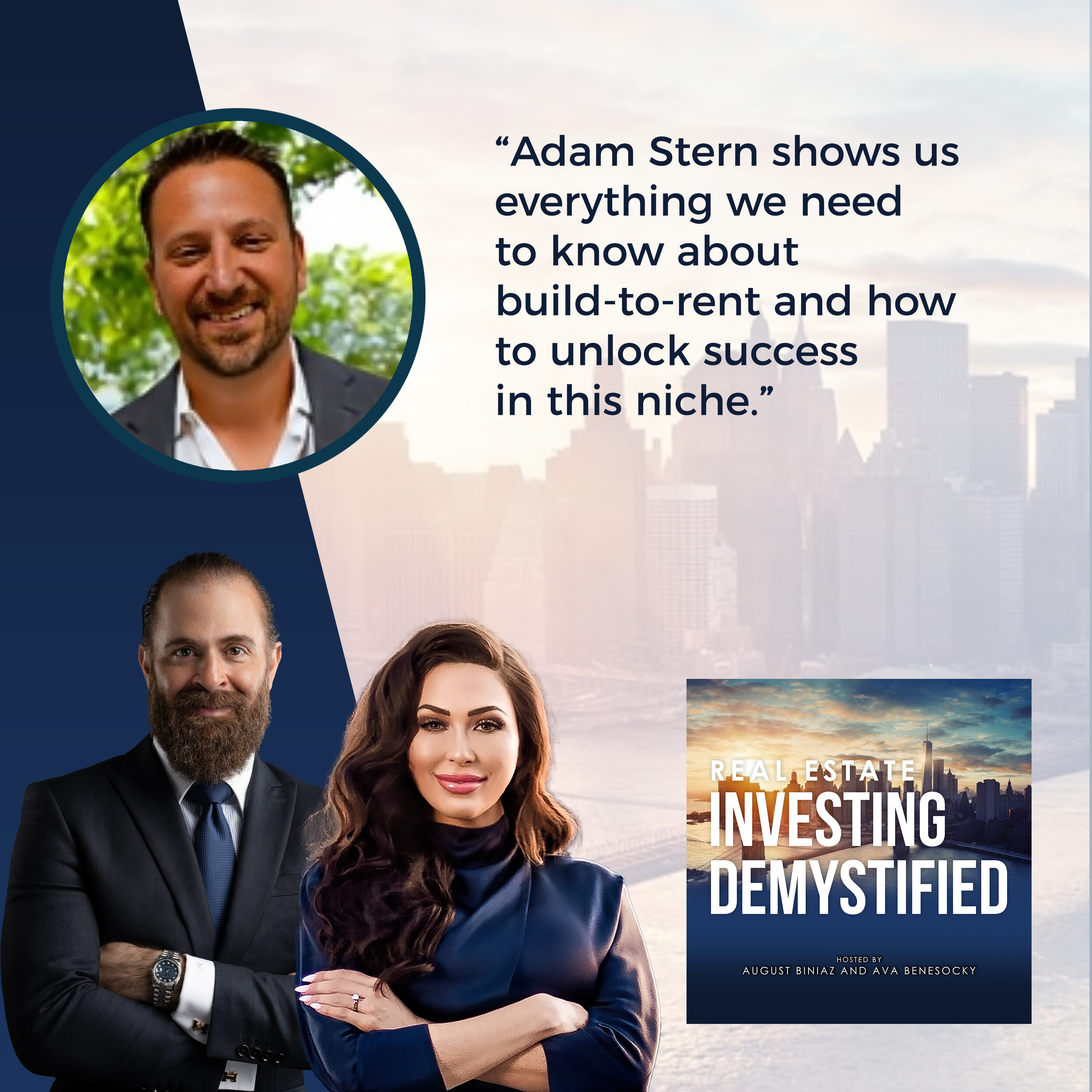

A housing trend is on the rise as it continues to evolve in the real estate industry. The shifting of housing preferences, rising homeownership costs, and demand for amenities and communities are some factors contributing to the growth of the Build-to-Rent space. In this episode, Adam Stern, the Founder and CEO of Strata SFR, reveals exclusive insights to unlock build-to-rent success. He also talks about the downside of having institutional interest in the housing market. Adam pivots into what he sees in the build-to-rent projects and if there are concerns for hypersupply. Why don’t you open yourself to this asset class and see what awaits you in rental space? Join Adam to learn more about him, Strata SFR, and the BTR space.

Get in touch with Adam Stern:

LinkedIn: https://www.linkedin.com/in/adamstern00

If you are interested in learning more about passively investing in multifamily & Build-to-Rent properties, click here to schedule a call with the CPI Capital Team or contact us at info@cpicapital.ca. If you like to Co-Syndicate and close on larger deal as a General Partner, click here. You can read more about CPI Capital at https://www.cpicapital.ca.

#avabenesocky #augustbiniaz #cpicapital

—

Watch the episode here

Listen to the podcast here

Important Links

About Adam Stern

As a real estate entrepreneur, Adam launched Strata SFR in 2020 after selling a previous company that he co-founded, OwnAmerica, which was one of the first sales platforms designed to market and sell Single Family Rental properties. Over his tenure as CEO and Founder at Strata, the firm has become one of the most visible and highly respected specialized real estate brokerage and investment companies in the ever evolving Single Family Rental and Build for Rent industry.

As a real estate entrepreneur, Adam launched Strata SFR in 2020 after selling a previous company that he co-founded, OwnAmerica, which was one of the first sales platforms designed to market and sell Single Family Rental properties. Over his tenure as CEO and Founder at Strata, the firm has become one of the most visible and highly respected specialized real estate brokerage and investment companies in the ever evolving Single Family Rental and Build for Rent industry.

Adam is a leading expert and sought after speaker and writer on the Single Family Rental and Build-for-Rent market. At Strata, he leads a team that provides guidance on go-to-market strategies for SFR Portfolio Operators, Builders and Land Developers who are focused on expanding their volume and revenue by servicing the ever increasing demand for Single Family Rentals (SFR), particularly from large scale investors that own and operate rental homes in US.

As an off-shoot from Strata’s core SFR business, Strata has become a powerhouse land and lot brokerage company, supplying valuable land positions to a network of builders that operate in the Southeast US. Adam is also an authority on the acquisition and disposition of SFR portfolios nationwide. He has helped facilitate SFR transactions totaling hundreds of millions in volume and was one of the earliest to recognize that portfolios of Single Family Rentals was a product type and that it deserved a purpose built, specialized brokerage service.

Adam is a father of four strapping sons, Lucas: Tyler, Jaxon and James. Husband to Ainsley, and is one of 4 brothers. He lives and works in Lake Norman, a suburb of Charlotte, and enjoys life on the lake, boating, wake surfing, playing poker, fitness and spending time with friends and family.

Unlocking Build-To-Rent Success: Exclusive Insights With Top Broker Adam Stern | Commercial Real Estate Game-Changer

It’s 2024. It’s our first episode of the year. We took some time off. Some exciting news on the personal side, August and I had our adorable baby boy, Atlas Cyrus Wolfgang Biniaz. There’s an amazing story behind the name. We’ll tell you guys one day. We welcomed him on November 21, 2023. He’s an amazing child.

What an experience that I thought I’d been through all in life but having a baby was an incredible feeling. We’re excited to be here.

One more thing, our baby search words are going to be real estate private equity.

He’s going to have the whole world on his shoulder carrying CPI. I always say this joke with my friends, “I’m going to raise my kid and educate him to go make somebody else rich. He’s going to stay in the house and help with the company. We’re excited about all that stuff.

You guys will meet him one day soon.

We’ll get into the episode. It’s been many months since CPI Capital has done a deal.

It keeps growing.

In retrospect, we seem like we’re pretty experienced and knowledgeable not having done a deal with a lot of firms in distress and finding themselves in bad situations. There was a deal we were looking at around, which was a Build-To-Rent and Single-Family-Rental or BTR and SFR deal, which we were buying in Tucson from a developer. We start into this asset class as that’s fascinating. Our guest for this episode is an expert in BTR and SFR as an understatement. We’re excited to have our friend on the show.

We were getting his opinion back if you can recall.

He was one of the first people I called.

We’re excited because we have the expert himself, Adam Stern. Here’s a little bit about Adam. He’s an expert in the build-to-rent space. He’s the Founder of Strata SFR, which stands for Single Family Rentals. He’s transacted on more single-family rental portfolios than any other professional in the SFR industry. He has helped facilitate SFR transactions totaling hundreds of millions in volume. He is a father of four sons. We know that he also has a lot of patience. We believe this interview with Adam will bring great value to real estate investors looking to learn more about the build-to-rent and single-family-rental asset class. Welcome to the show, Adam. We’re happy to have you here.

Thanks. How are you doing?

We’re doing great. Let’s get into things. Start by telling us about your background and then how you started in the build-to-rent space.

Mine is an interesting story because I always grew up in the early parts of my career in the real estate industry. I started my career by selling title insurance. I was a title insurance rep for a little while. I had brave out into my business, which I launched in early 2007 right before the crash, selling securitized real estate investments called Ticks and VSTs. Eventually, I ended up launching a company with my mentor. It was called OwnAmerica.

Our big idea at the time was there was a housing meltdown and real estate agents had no idea how to sell a home as an investment. We put an online training program on the web and then sold it to real estate agents, showing them how to sell a home to a real estate investor. A company called Invitation Homes backed by Blackstone raised $1 billion on Wall Street to buy foreclosures and show them in our rental properties.

They said to my partner at the time, “Those guys are going to be buying a lot of properties to real estate agents. They should be using our real estate agents because our guys know what a cap rate is and know how to calculate a return.” We ended up changing our strategy from training agents to already 2,000 agents in the Southeast. We built some technology that allowed a big institutional investor, we didn’t grab that, the Blackstone account but we had a bunch of other ones including American Residential Properties, Tricon and a few other institutional investors plug it into our network where we essentially ended up being an acquisition service for those big REITs.

We ended up selling $300 million to $320 million of SFR real estate source buyer agents to these institutional investors. That was great business because it let us get to know all the buyers who raised money to buy SFR assets as they entered the industry. At the beginning of the industry, which was 2009, there was a handful of big buyers. We were at the front doorway as more of these buyers ended up coming into the industry and as the industry expanded.

What ended up happening was a lot of the firms that we had, that were doing their acquisitions through us, ended up internalizing their acquisition program. By talking to a lot of owners, I ended up realizing that there were these owners who owned 10, 50, or 150 properties. They had no brokerage service that could help them sell their portfolios. Portfolio brokerage was a thing or at least it should have been a thing. We turned OwnAmerica into a technology platform, which we were, and SFR portfolio brokerage essentially. I spent the next few years getting to know how to find portfolios, analyze them, and broker them between private owners and institutional investors which I came to know so well.

I went from maybe a handful of buyers to a dozen buyers to knowing hundreds of these buyers with all kinds of different strategies. We ended up selling the business in 2018 to another company. The whole built-for-rent thing started taking shape. It started picking up steam in 2018 and 2019. If you didn’t know the genesis of build-to-rent, it started happening in markets that made more sense to build a new home than it did to buy an existing home because new home prices in places like Phoenix, Arizona, and Las Vegas in certain key markets put the home price of an existing home above its replacement value.

Build-to-rent started happening in markets where it made more sense to build a new home than buy an existing home. Click To TweetAll these firms that looking at these markets and saying, “Why don’t we start engaging builders,” sell us new construction homes, individual homes but also single site projects that are in a contiguous subdivision that got known as build-to-rent. I realized at the time that no builder knew as much as I did about how these funds operated. I felt like offering a service to these builders that helped them gain access to this new buyer group, which were private equity firms and operators to sell their inventory to those groups would be a good thing.

We found a niche in build-to-rent by focusing on regional and medium-sized builders that had a pipeline of projects that needed some guidance on finding out whether the project would work as build-to-rent. Why or why not? Ultimately if it did work as build-to-rent, how to gain access to an audience of potential buyers that can help them get the best price for their assets?

That’s the company that I launched in 2020. Strata is an SFR and build-to-rent brokerage that focuses on helping builders find some knowledge and insight into the build-to-rent segment. We appropriately help them sell their assets to our ever-growing network of funds. We also do SFR portfolio brokerage and do the thing we always did, which was also helping those portfolio owners sell to similar investment companies. That’s how I landed here with you.

What a tremendous story. Thanks for sharing that.

We launched many years ago.

In my research about the start, the genesis as you call it, of BTR as SFR or build-to-rent and separating that from SFR or Single-Family-Rental portfolios, it did start in that post-GFC where Wall Street got involved and started buying homes pennies on the dollar. Their plan was waiting for the cycle to turn and for them to exit it in a matter of a couple of years. That was their business strategy. As they would hold these single-family portfolios, they noticed that they started performing like multi-family. As you explain, as soon as the cost of building a single-family home detached home in the community, started being less than buying apartments for these institutions. They start building them and partnering with other builders. We’ll get more and more into that. There are a couple of our questions come out of the box. It’s a great storyline.

After telling your story, I want our readers to truly understand the difference between build-to-rent and single-family-rental portfolios if you could.

Single-family rentals are not a new thing. People have owned single-family rentals. Mainly, it was a business that was almost entirely owned by small mom-and-pops. I remember at OwnAmerica, we had a pyramid where the broadest part of the pyramid, which was 90% of it were people that owned one rental home and then you had the next smallest, 2 to 5 rental homes, which was 5% of the pyramid, then people that own more than 10 were an extremely small slice.

Originally, the idea behind single-family rental as being an institutional asset class was if larger capital stacks could partner with operators that could essentially roll up larger portfolios of scatter site, single-family rental properties, which is what we call a portfolio when it’s one property here, another property here, and it’s all generally in one market but they’re scatter site, which means they’re relatively hard to manage unless you have some scale.

The big thing is it was a distress play at first and then it was contemplated as a trade, “I’ll buy for this and then sell for this.” It eventually became more of a, “How do we operate this as a business?” The more scale you get in owning single-family homes, the more efficient you become in managing them, the lower your overall expenses get, and the higher your returns get. What Wall Street realized was comparing single-family homes at scale to multifamily, single-family became for a little while a higher return play for the same operational prowess that you need to have to manage that many homes.

As I’ve seen the industry evolve, what I see is still the majority of single-family homes are owned by people who own one. You have this other swath of people that own 2 to 5 as being much bigger. You have more people owning that number of homes than ever before. You’ve got a lot more people that own between 10 and 100. You have the biggest investors who own hundreds or thousands of these homes. The presence of institutional investors in the single-family rental segment means all the smaller fish have a destination. If you get a portfolio, if you own one, the opportunity for you to sell to a smaller investor that owns 10 is more prevalent than ever and it gives you an exit opportunity that you never had before.

If you own 10 and you can build your portfolio to 100, you’ve got an opportunity to efficiently and for a very good price sell all those homes in one slice or swap to a big institutional investor. If you get to the top of the pyramid where you own hundreds or even thousands, you’ve got a better chance of being able to exit your portfolio in one fell swoop to an even bigger player. You’ve seen this consolidation play out year after year to the point where news articles come out as Blackstone went under agreement to buy Tricon residential homes, which they own 34 validation.

I help the consolidation happen toward the middle part of the pyramid where if someone owns 10, 50, or 100, being able to find one investors probably easily enough could read a news article and call them up and say, “I want to sell you my portfolio.” Being able to sell it efficiently means you’re not just serving up to one investor but to a universe of investors that has to compete for it in a certain way so you know you’re not leaving any money on the table. That’s what I help out with.

In a long-winded way, it turned into an industry of very small mom-and-pop shops and a relatively small group of professional institutional investors. What it’s turned into is the mom-and-pop and then the ever-increasing number of professional and institutional investors where new technology and data are making them better and better at finding the properties they want to buy, building the portfolios they want to build, and operating them more efficiently.

Ultimately, it’s a good thing for everyone involved. It’s a good thing for people who own portfolios because they have options about how to sell it and who to sell it to. It’s a good thing for renters because operators becoming more professional and they’re creating a better product to live in and to raise a family in. That’s the way I look at the industry. I’m playing a role in helping smaller people consolidate with larger ones and helping source good opportunities for the larger ones who can operate these portfolios efficiently and create better housing stock for renters everywhere.

I get what you’re saying and aligned with what you’re explaining here as far as the advantages and supply it creates. To be the devil’s advocate, there are some movements and talks on a government level like, “Wall Street is getting involved in single-family homes and there’s making it difficult for the everyday person to own a home.” We come from a city called Vancouver in Canada, where a median home price is over $1.5 million and a medium income is around $100,000.

It is very difficult for people to afford to buy a home. The government is trying its best to make housing more affordable. How about conversations like that or talks? What is your response to Wall Street getting involved in the new generation not being able to afford a home because they’re outbidding, even though I know that the data proves otherwise, which the percentage is way smaller but please tell us.

I watch Canadian politics all the time. The guy that’s running against the rule is Javier. I love that guy and he’s got a lot of good ideas. I don’t necessarily agree with the way Trudeau has managed the Canadian economy. I see what’s happening in Canada. I’m not Canadian. It’s a little bit detached for me but you can correlate it to the movement in SFR. I understand it.

The way I understand the movement is having an institutional interest in the residential housing market is a bad thing for average everyday Americans because they can’t compete against these big deep-pocketed institutional investors. I have to toe the line because I play a role in helping those institutional investors gain more assets in the market. I’ll be honest, I’m a bit torn between understanding the movement of does institutional buying in a market limits the buying opportunities of people who want to own homes. It does.

If you’re listening to any one of the large CEOs and publicly traded REITs, they’ll normally say, “Institutional investment only owns 1% or 1.5% of homes nationwide.” Everyone who understands the industry knows that they’re only buying properties in 10% of the country. In markets like Atlanta, Charlotte, Jacksonville, Orlando, Houston, and Dallas, they own an outsized number of a certain type of house in certain areas of those markets. As much as in Atlanta, institutional investors might own as much as 30% or 40% of certain neighborhoods, which makes it harder for everyday people who are looking to compete for those homes to buy and live in. It’s a struggle that’s going to continue to happen.

I do think regulation is a healthy thing. Institutional investors do play an important role in creating good housing stock and that option for people to live in better quality houses. I’m torn. I see both sides of the fence. Do I think unfettered institutional presence in the residential housing market in America should be unfettered with no regulation? No. Regulation is needed but I also think it needs to be tempered with the good that the institutional investors bring to the market.

Having an institutional interest in the residential housing market is a bad thing for average everyday Americans because they can't possibly compete against these big, deep-pocketed institutional investors. Click To TweetI’ll throw my idea here. Anytime you get institutions getting involved, there’s a level of greed that gets involved. When you have greed, you have a potential of oversupply or hyper-supplies. It might work out to the homeowner’s benefit when groups get involved and overbuild or over-purchase. Real estate gets cyclical so they might hit a hard cycle and have to offload those homes.

The way I look at it is the purpose of a company, whether it’s Microsoft, Apple, or Tesla, is to turn a profit. Naturally, when you get companies involved, like in the homeownership market, they’re incentivized to generate as much profit as possible. One of the downsides to having institutions like be in a market like Atlanta for example, they’re going to do everything in their power to consistently raise rental rates over time.

If they own enough properties in the market, they’re going to essentially set those rental rates in a market where they own an outsized number of properties as opposed to what happened in the decades past, which is those properties were owned by his mom-and-pops who cared about a profit but they didn’t have stockholders to answer to. They might not have raised rents over a 5 or 10-year period. Rents didn’t rise as fast, which is what’s happening where when you’ve got these big institutions that own an area, they’re consistently improving their properties and maintaining them to a very high standard to raise rents consistently.

It’s a good thing from the stockholder perspective and institutional perspective because they’re seeing their return and their stock prices get higher. I can also see it from the other side where rents are becoming more expensive in no small part because of this presence of institutional ownership. A happy medium between the market will speak and eventually, rents will reach a rate where they can’t keep increasing at the same rate. The market will dictate that. I guess the question is, “Will it decrease the number of people who are able to afford those homes and force other people who want to rent those homes into lower-quality rentals?”

Build To Rent: Rents become more expensive in no small part because of institutional ownership.

To me, that opens up a whole other opportunity which is coming out with more affordable rentals, being able to come out with a different product type. That’s where the industry’s going, coming into more niche asset types within the SFR space like high-end rentals, higher-priced A properties, medium-price B properties, and even what they call workforce housing properties that run out for the lower end of the rental spectrum. They’re not as nice and as good of areas in terms of crime and schools but they’re more affordable. The market will dictate whether or not how that’s going to play out. The better or rental stock that’s out there forever, the better it’ll be.

Thanks for describing all that. I’m going to switch it up a little bit here. Our firm is focused on multifamily value add but we’re very bullish on the build-to-rent. Could you differentiate between, as you already did, the build-to-rent and single-family rental portfolios and then your conventional multifamily property?

I talked about single-family portfolios and what they were. The idea of build-to-rent is if you can get contiguous subdivisions of homes that are all owned by an owner or an owning entity but are managed like a multifamily, you can create a good community atmosphere and nice amenities, and compete well against multifamily. There are a few iterations of that from the most traditional build-to-rent, which is what they call horizontal apartments. That’s generally one community.

In build-for-rent, you can create a good community atmosphere if you can get a contiguous subdivision of homes owned by an owner or owning entity but managed like a multi-family. Click To TweetSometimes it’s even on one lot where it’s just one lot and they’re not subdivided into individual lots. It’s always going to be owned as a rental community. Tenants go in there. They lease it up like an apartment building would lease up. They stabilize the rents, get the operational cost in line, and manage it like a multifamily. It’s the same thing as a multifamily. It’s just a bunch of houses or town homes as opposed to multifamily.

In some cases, it can have a pool.

In most cases, a property that’s big enough like 100 units or bigger will always have amenities because if it’s a community that’s that big, the amenity has a cost but when you spread it over that many units, the amenity cost ends up being a relatively small part of the overall unit price. When people talk about build-to-rent, that’s what most people are talking about. You also have other iterations of build-to-rent, like smaller communities that are maybe 40, 90, or 100 units. They’re not big enough generally to have an amenity but they’re smaller. They’re generally what you get when you go into infill areas.

When you go into a market and you want to buy a build-to-rent that’s sandwiched between a multifamily and a retail corridor and a downtown with offices, it’s very hard to get 30 or 40 in an infill location like that. What a lot of investors look at is if it’s an infill location on a location or a good proximity to population centers or retail job centers, they’re fine owning and managing those as single site build-to-rent.

Generally, they’re going to be owned by either larger investors that have other assets in the area and they can manage that property in conjunction with other properties they have, whether they’re small or built for rent or even scatter site properties or smaller investors that are fine with owning that small project. That’s what we see. Bigger projects are generally in more suburban locations. I call them outfill on the bleeding edge of where the development’s going and then you have these smaller communities that are generally more infill that.

On the property that we were going to be taking down in Tucson, it was an infill piece of land. It was about 70 homes. It was interesting for me to go to investors with this new asset class build-to-rent and say, “This is a piece of land. We’re going to be building properties and then renting them off one by one. It’s going to operate exactly like a multifamily.” It was smaller in the institution when it had a pool and all the amenities. This one didn’t have amenities.

It was hard for investors to be like, “It’s going to be a horizontal multifamily. Look at it like that.” They were right away like, “Where’s the pool, fitness center, or leasing office?” They were so educated on how a multifamily operates but they had a hard time wrapping their head around this build-to-rent asset class when presented with the deal. It took a lot more explaining to do as we presented it.

What convoluted this deal further was the purchase contract as well as a forward purchase contract that we were going under contract, paying a deposit but only purchasing the homes and the certificate of occupancy, which was something that we had to explain to investors. When you’re dealing with retail LPs, the confused mind says no. They’re coming to the situation and say, “Do I want to invest with this firm or leave my money with my money manager or financial advisor?”

Going off of something that Adam said, the story I’d like to tell my investors on this particular deal we approached a builder who was planning to build one by one and sell it off as a single-family home. It was very interesting when we approached him. We said, “We want to buy all 70 homes from you.” He’s been in the business for a very long time with his certain business model that he was used to doing. He was excited about, “There are groups that are going to come in and buy the whole portfolio that I’m going to be building.” It’s a unique situation.

It lowers the risks but it also caps the profits they can make because when they sell it one by one, they could sell depending on where the market is going.

I want to comment on a few things. Part of the challenge of smaller developers and builders trying to sell their properties as build-for-rent is there are a few things for you to consider, which is who are you going to sell it to or who are the buyers out there that are looking for that kind of opportunity? If you have a 70-unit property in Tucson, which is not a market a lot of institutional investors are in, the question that they’ll have is, “Do they like the market? Are they sold on the market?”

If they’re already sold on the market and they’re already in the market, then that to me is the best buyer group, Someone who is already sold in the market may own some other assets, multifamily, or real estate investment assets, and would like to add a 70-unit bill for rent to their portfolio. What you’re not going to get is large institutional investors that haven’t decided on Tucson because even if they get convinced yet, “I like this market,” because you talked about it but 70 properties aren’t going to let them get enough scale to buy this deal.

There’s a lot of thought that goes into, “I’m a broker. I think about how saleable a project is. You’re a principal. You’re already invested in it.” I look at it from the perspective of, “Is there a market for it?” That’s the question I ask myself first. “Who are you selling this to?” For smaller projects, that is generally going to be existing investors that own assets in that market or smaller investors that don’t have these huge checkbooks but don’t need to get scale and would be happy owning that investment. The problem that a lot of investors face, especially with smaller developers like you guys is that you don’t come out with hundreds or thousands of opportunities.

You come out with maybe eight projects every year. Is the juice worth squeezing? If I get this deal done and I walk down the path and make the deal, you guys might turn around and say, “For the money we’re making out for selling it as a forward contract to this investor at CEO, maybe we should develop the lots and then sell the lots to a national home builder. We can make as much profit doing that with less hassle.” That ends up happening quite a bit when I walk down the path in a small build-to-rent with a smaller operator. All of a sudden, they look at the numbers and are like, “Can we sell the lots?” The answer is, “Yes, we could sell the lots.”

That’s what we’re going to get to our next question here. You’re answering it. Let’s discuss different business models and the buyer profile that exists within the space. For example, what type of groups buy land, entitle it, and then what groups build vertically? What groups take it to stabilization and send it, sell it to the institution, a private equity firm, or syndication? Are there groups that keep the property long-term and their business plan is to build, stabilize, refinance, and keep it long-term?

Maybe you can talk to us about different business models that exist within the build-to-rent asset class outside of Single-Family Rental or SFR portfolios as as you discussed but particularly build-to-rent. You could entitle land and sell it to an institution. You could build, stabilize, and sell, or keep it for yourself and refinance long-term. What are you seeing in this space? Who are the buyers of the different business models?

There’s a whole value chain of people who are involved in a build-to-rent deal. If you segmented them off, it would be the land developer first. Land development and entitlement are probably the hardest part of the equation. It takes a lot of experience to do it well. There’s a huge amount of risk in it. I’m afraid it’s becoming a long-lost art unless the current people who do it teach the next generation how to do it. It’s going to get hard soon to find good land positions. That’s the first piece of the puzzle.

Build To Rent: Land development and entitlement are the hardest part of the equation. It takes a lot of experience and a huge amount of risk to do it well. So, teach the next generation how to do it.

Have a firm that knows how to search out raw land and how to take it through the entitlement process. For those of your audience who don’t know the entitlement process, it is doing the research on the land, including all the geotechnical surveys, traffic studies, and feasibility reports to figure out whether or not an asset type like built-to-rent would fit well there.

When all that money is spent and that’s figured out, creating the site plan and then taking it through the approval process which in some markets can be very arduous and long-term and cost a lot of money, eventually the land will be considered what’s considered fully entitled. It means it’s zoned correctly and all the research has been done on it. You’re ready to start the next phase which is building the lots. That’s a whole other skillset. That’s an actual company that can come in.

Based on the work that’s been done by the previous firm, understand what units need to be built after entitlement. Generally, during the entitlement process you submit CDs, which are the Construction Drawings that need to get approved, which outline the units you could build there. Once all that’s done, it takes hard machinery to start leveling the land and making it ready for vertical building. There’s a lot of expense and risk in that. That’s the middle part as you are taking it from the entitled land to the finished lots.

It is called shovel-ready. I’ve heard that term lots where it’s shovel-ready ready to go vertical.

There are a couple of different terms where if a person says it’s permit-ready or ready to move durst, that means it’s ready to start building the lots. People could say it’s shovel-ready and they could be talking about how a raw piece of land is ready to start building the lots. Sometimes when people will say shovel ready, they’ll say, “I’ve got a finished lot. It’s complete. It’s a lot and we’re ready to go vertical.”

My understanding of shovel ready means it is ready to go vertical and also the entitlement for Canadian readers reading this. It is a feasibility study and rezoning. If you’re doing the feasibility study to see if it makes sense to build on it and then rezoning through the city, that’s what entitlement means for Canadians.

It’s similar to us. Entitlement is paperwork, essentially. The lot building is moving around dirt and getting the lots ready. The vertical component is building the units. Once you’ve got the units built, generally as a build-to-rent, you have to hand it off to an operations company that’s going to start the lease-up process, which you’ve done well. You start the lease-up process well before the first units are ready. When the first units are ready, hopefully, you have a VIP list or a list of of renters ready to start moving into those units.

Once you get the units built as a build-for-rent, you have to hand them off to an operations company, which will start the lease-up process. Click To TweetThis whole value chain has to come together well maximally profitable. When those things don’t come together as they sometimes don’t and you have lag time between the different parts, the more time that passes in the development or leasing of a project, the more money it costs you because you’re losing revenue and spending money on construction and other service providers that are involved in that entire value chain.

If you look at that entire process from entitlement through building the lots, homes, and leasing the mouse, there can be firms that are out there that are considered vertically integrated. We’re working with one. We’re selling a project in Huntsville. It’s a company called Jim Chapman Communities. He’s built eight communities in different markets where he finds the land, goes through the entitlement process, builds the lots, builds a very specific product, and manages them with third-party cold-range water. They’re vertically integrated. That’s the highest level of building for an operator that there is out there.

They don’t sell it. They keep it for themselves and refinance at some point.

What Jim did was he stabilized it and then sold those stabilized properties to an end investor who is going to own it for the next ten years. Some of those vertically integrated operators might not stabilize it. They’ll bring it through to finished units and allow the buyer to buy it for a better price. The buyer’s taking all the lease-up risk. What ends up happening in a built thread project is when you have non-verbally integrated operators, sometimes what you have is people filling each role and trying to maximize the value of what they’re working on.

You’ve got a developer who doesn’t ever intend to build the lots, they’re bringing it through entitlement. They have the opportunity to sell those. They’re called undeveloped lots or paper lots. They can sell those lots to a build-to-rents buyer who can then develop it or to a builder who can then build the lots. A lot of times what you get are developers who are fine building the lots and even find the land and entitling it but don’t ever intend to build a home. All they want to do is sell the finish lots and they’ve got the same opportunity, sell the finish lots to a builder or a build-to-rent firm. It continues.

If you’re a builder, sometimes you don’t do entitlement or build lots. You look for finished lots and build your home. You have the opportunity to sell that home in one swath to an investor as a build-to-rent or to individual home buyers as individual units. There’s a lot that can go wrong and right. There are a lot of different structures to help build-to-rent deals come together. That’s part of what I try to figure out in my business, which is who’s the seller? What are they trying to accomplish? What’s the best execution for what they have their hands around and what they own and control? Is that worthwhile for me as a broker to take on and find a buyer for it? What are the chances to sell people to find a market of willing buyers interested in that product type in that structure?

We’re in a syndication space with syndicators of our deals. We’re launching a fund as well to allow Canadians to be able to invest in US multifamily as the market turns around. Let’s talk about groups that utilize the syndication model. They bring on LP equity to acquire and build-to-rent. What is the door count that these types of groups look at? Are they buying 40 or 300 doors, like these big institutional types built to rent with the amenities? For example, the multifamily value add space, which we are in is called the middle market. We’re buying that 100 to 350 doors value add, building in ‘70, ‘80s, ‘90s, 2000s and what have you. What is that sweet spot for syndication groups or are even seeing groups syndicating build-to-rent?

We see it all the time. I don’t look at the large institutional investors like Progress Residential, American Homes 4 Rent, or Invitation Homes. They don’t syndicate. They have money that’s been raised billions of dollars. They’ve got these pots of money and they have to deploy it. When they deploy it, they buy the assets, the operative, and then they refinance them. They’re not syndicators. What you’re talking about in my space are small operators very often that go out there and find a deal. Generally, they could be smaller deals or larger deals.

When they find a deal, they’ll call me up and say, “This fits our model.” They’ll write me an LOI. I’ll ask, “Are you looking to raise money on this or do you have captive capital to do this deal?” For me as a broker, capital is always better because it doesn’t leave the question mark of, “Can you raise the capital to get the deal done?” The firms that I work the most with that I know are going to go out there and “syndicate it,” most of what they’re doing is not running open syndication.

They’re taking that deal and syndicating it to their closed network of high net with individuals, family offices, or private equity investors. They generally have good agreements with these firms already penned or good relationships like, “I’m a private equity firm and I’m hooked up with an operator. I’m waiting for this operator to bring me a deal. When they bring me a deal, I generally like it because they know what I like. They know how to find good deals and operate those deals.”

That’s the most prevalent syndication that I see where it’s an operator that has a small network of investors. They find the deal, lock it up, go out there, and get the money from their network of investors. The good ones, there’s no question that they’ll be able to raise that money. If they like the deal and write me an LOI, it’s almost 100% that they’ll be able to go out there and get that money from their investors.

You have smaller investors that don’t necessarily have that high-quality private equity family office or institutional investor capital where they might look at a deal but they have to openly syndicate it, which happens a lot in middle market multifamily, which is firms like yours. You’ve got good experience so you know how to find the deal, how to structure it, and how to do the math on it but you might not have 25 willing-ready high net worth or institutional-type investors backing you.

You might have to go out to a network of high-net-worth individuals or even family and friends. From a seller’s perspective, that can be a great thing when you find a good one because they’re a reliable buyer and are generally more opportunistic, meaning they don’t have to find a very specific deal to make it work. They go buy anything. It also comes with risks. Sometimes those guys go out there and strike out. They try to raise the money but they can’t. That’s what I see from top to bottom.

Sometimes, people go out there, and they strike out. They try to raise the money, but they just can't. It comes with risks. Click To TweetWhat’s the door size that these two groups look at?

The smallest I’ve ever sold in terms of build-to-rent rent was 29 properties in a single-site subdivision. It was an infill location. It was in Charlotte. We ended up selling to a fund. He had a group of close friends that were all high-net-worth individuals. He went out and ran that syndication. The smallest is 30. It’s hard to spend the time and energy on those who want to do a smaller deal than that.

You’re more focused on the equity side. I’m more focused on the business model. What number of doors makes sense for there to be economies of scale?

I’m not on the equity side. I’m on the brokerage side. I have to find the money and the assets and figure out how to put them together. The size deal that’s most attractive to me is 75 to 125. That means size because it’s big enough for the institutional guys to maybe do that deal but it’s also small enough that you’ll appeal to firms that have more limited capital. Generally, at that size, economies of scale start to take shape.

A small number of vacancies affect the overall performance. You’re not building many units in one place where you’re afraid that there are not enough renters in that area that’ll be able to take that product. When you get larger than 25, you start looking at how many people live in that area, how many people are going to that area, and what’s going to be the future demand for rentals in those areas. That’s a big risk.

What’s a competition like when you bring a deal to the table, 70 to 125 units? Are there lots of competition?

It depends on the market. We have that question coming up later on as far as how the market is afterward but it depends on the market I’m guessing.

Let the expert answer.

It depends on the market but more specifically, I consider myself a market maker. I’ve spent the last many years of my life cajoling this network of buyers into my market. When I find a product that’s worth doing, like ones that I’ve done, if I do my job well as a broker, I’ll know out of the 300 firms that I have my database, which ones own assets already in Charlotte and are currently funded to buy more. Even beyond that, how well they’re doing in their current properties, and how their appetite might be better if they’re doing better in that market? I spend a lot of time figuring that out.

You always have usually typically more than two people who want to buy the same asset.

I don’t take a deal unless I know I have at least half a dozen buyers.

Let’s try to bang through the next few questions.

I’m excited about the next question. Let’s discuss BOV or Broker Opinion of Value. When you have a seller approaching you with a deal that they have, how do you underwrite the deal to come up with your BOV? Do you have a rule of thumb that you use?

Is it the same as multifamily? Is there a cap rate or NOI approach? Give us a crash course on how you look at deals in build-to-rent space.

When it comes to build-to-rent, they’re not built units. They don’t use cashflow. We use a term called yield on cost, which is the same thing as a cap rate. It’s the return you’re getting from the money you’re putting into a real estate deal from the cash you’re putting into building the units and eventually getting them to be operated.

When I look at a build-to-rent end deal, I try to talk to as many owners and operators and not marketing, try to figure out where they’re buying or what cap rates they need, yield on cost that they need to make a deal make sense. For example, in Charlotte, if someone’s buying a stabilized build-to-rent deal, I could probably be okay pricing it to a high 5% or low 6% cap rate. That used to be low 5%. We’re giving a high 4% cap rate back in 2021 but for a stabilized deal, I’m looking for a high 5% to 6% cap rate.

If it’s a deal where I’m selling vacant units that aren’t stabilized, what I do is use data sources like CoStar, Zillow, and Redfin. I pull as many AVMs as I can to try to figure out what the value of those units is on the retail market because I need a high watermark. I need to know what the value of those units will be if you sell them retail. I go through the same process of pulling rental rates from all these different data sources to try to figure out what the property might run for. When I have the value and the rental rate, I could put it to a pro forma and then figure out generally if it’s a build-to-rent deal, what the yield bond cost is given my rental rate.

If I need to hit Charlotte for a vacant property, I need to probably hit a 6.5% cap. I need to price it at this much per unit. When I go to my seller and say, “To hit a 6.5% yield on costs for this deal, I need it priced at X number of dollars per unit. I did the research and the retail value is Y number of dollars per unit. There’s a $30,000 differential right there. What do you think?”

“I own 100 properties and you’re telling me to take a $3 million haircut. I don’t think it’s worth it. I’m going to end up going and selling them retail.” “What would be comfortable to you?” “I want to sell it at retail.” “It’s only a low five-yield on cost. No one’s going to buy that. It’s not worth my time or your time.” That’s the way I look at it. Gather all the information, price it, figure out what the rents are, talk to a lot of buyers and owners in the market, figure out where the cap rates or the yield on cost needs to be, and then price it appropriately.

A question for you again on this topic. You can do a role-play if you want. I got a bill-term property. It’s not stabilizing. You trying to give me a BOV and then you come with your findings. I’m like, “There’s no other build-to-rent rent nearby. You’re comparing it with multifamily and single-family rental. My property is different.” What is your answer back to me as a build-to-rent developer who’s saying that the information you brought is comparing single-family and multifamily, which is not my asset class?

I would ask them to go into the role of a buyer, try to imagine themselves as a buyer, and give me the best-supporting evidence that they can come up with to give me a rental rate. I’m telling you the data sources that I’ve identified and my logic behind them, the best way for me to price this deal is by looking at close-by multifamily properties. That’s a good way. Looking at the scatter site, it’s individual homes that are renting out and then using that as a benchmark or even going into another similar market with similar products, demographics, and school scores and then using those rents.

Build To Rent: Imagine yourself as a buyer and find the best-supporting evidence to come up with a rental rate.

It’s more of an art than it is a science and everyone’s going to have their opinion. What I usually do is form my opinion using my best logic. I bounce that logic off the owner. I said, “This is what I think. What do you think?” Some of them are like, “You’re crazy. My community is a special flower in a snowflake that’s unique in itself.” They’ve got all these reasons. Sometimes they make sense and convince me, “This unit that I thought would rent for $1,200 a month, maybe it could rent for $2,000. Am I going to be able to convince a buyer of that? Do we have any empirical evidence to support that?” Very often the answer is no.

They’re asking for a flyer and have some faith. I always tell them, “I’m happy to have faith. I’m a faithful guy. When I’m managing $10 million, $30 million, or $50 million, a lot of times, faith and judgment don’t come into that goal. There has to be empirical evidence. We’ve got to come up with good support for whatever rental rate that we’re saying it can fetch.”

Let’s discuss oversupply or hypersupply in the BTR and SFR space. As this asset class becomes more and more popular as it has been and more capital starts to flow into this asset class and the sector, are there concerns for hyper-supply?

We’re seeing in Atlanta or Phoenix where it’s common to have these types of build-to-rent projects. What are you seeing out?

This is where technology is playing a big role because before you had all these large data aggregators, you were trying to figure out how many units were being rented in a market or a submarket. It’s a relatively hard thing. I remember back in 2009 when people were trying to figure out what the rate that units were being rented at, they were pulling property managers and asking them, “How many units do you have in the market? Can you tell me how long to get sold?” If the answer was less than 30 days, it was a go. It was more than 30 days. It was a big risk.

Before you had all these large data aggregators, figuring out how many rented units were in a market or a sub-market was relatively hard. Technology plays a big role. Click To TweetYou’ve got all these data suppliers like HouseCanary, Zonda, and CoreLogic that have aggregated this information. You could go and look at how fast units are renting and what the absorption is. I’m not an expert on this subject by any means. What you generally do is find out the rental rate. Did my operators do a fair bit of research before they asked me for a deal in Atlanta and they defined their buy box for me? They already decided that this area is where I want to be because it has a good absorption rate in terms of rentals.

If you’re trying to figure this out for yourself, I look at some data providers that have rental absorption rate data as specific as maybe a neighborhood or a submarket in a ZIP code. There are a lot of cool data suppliers out there where if you specifically look for what data suppliers offer, things like helping you find out absorption rates for rentals in a submarket, that would be a good place to start. A lot of that work’s generally done behind the scenes and what I’m doing is talking to a buyer that already made the decision to buy in this area.

When I have a project that I’m pitching to a fund that doesn’t own this area, that’s a big question they have. Usually, I’ll have to go and find that data or at least ask the seller if they’ve done that research already. A lot of times, they haven’t. That’s the reason why a lot of projects don’t sell. The data’s not there by the seller to support how good or how well those rentals will rent. It doesn’t end up going anywhere. Sometimes it takes a good broker like me to do that legwork and it’s not very hard because there are data providers out there that have that.

How about gut feeling-wise? Do you feel there’s a market where there’s a potential of hyper supply for build-to-rent?

I look at some of these markets that have been in play with institutional investors like Charlotte, Atlanta, Orlando, Jackson, and Tampa. There’s a danger of oversupply in areas where they’re building lots of rentals in one single area. Even before one project gets built out and leased, another project is being built. That’s a real concern. That’s usually happening in two locations.

In Jacksonville, they can build as much as they want because it’s the largest landmass city in America.

If you build on a 5-acre parcel of land in infield Jacksonville where you have a multifamily down there and there are houses all around, there’s no chance that if you build-to-rent and price it appropriately you’re not going to find renters. It’s a different story if you’re way to the North and there’s farmland all around. You’re expecting people to drive there whether or not you’re building too many and whether that’s going to affect your vacancy in your rental rates.

Your answer is it depends.

Let’s talk about big players like D.R. Horton. Are they involved in BTR and SFR? If they are, are they building and selling at stabilization or are they getting involved in managing properties and renting them out themselves?

I focus most of my attention on medium-sized builders. I’ve intentionally stayed away from trying to get listing opportunities from the big national production builders but from what I understand, I believe big production builders like D.R. Horton have partnerships with institutional rental operators. I don’t know well enough to espouse there. I’m not going to talk out of school. What those biggest big production builders are doing is forming partnerships with large institutional investors where they’re being the supply chain for those institutional investors, selling those properties to those institutional investors maybe in a joint venture, and then managing them over the long-term.

I see those big firms have built for end experts on staff that do what I do. I’ve generally stayed away because those guys hire a full-time Adam Stern to go look for the next build for end project form programmatic relationships with these institutional investors where they know exactly what those the investors are looking for and they got a partnership with them. That’s about all I know.

I don’t look for them or do business with those guys. I do sell to those guys when I have a lot of listings. They’re very often like the buyers for the lots but most of them aren’t buying them as built-to-rent. Most of them are buying them as lots build homes on. That’s about all I know about larger type builders like D.R. Horton, LGI, and Pulte. They’re playing principle-to-principle with large institutional investors.

I’ve seen a D.R. Horton deal that hit my inbox which was 140 units that they had for sale. It was not occupied.

Is it one community?

One community.

They were selling all the units.

They were selling in one shot. It was very interesting. That’s what I saw. Let’s move on to the next question. I was listening to you on another show and you talk about how one of your strategies is reaching out to developers who do build communities of homes. You say, “There’s an option for you to sell these as a portfolio as a community to one buyer,” which historically they didn’t know was possible. They do a single home built-for-sale project and you say, “I have these buyers that come in.”

It goes from this strategy of them building a community and they were planning to sell them individually but then they sell it to one buyer who then turns them into horizontal multifamily and rents them out calling that same build-to-rent space. I’m sure you’ve done a bunch of these. We were involved in one as we talked about. Do you ever see it go the other way around? Do you ever see a project initially being a build-to-rent project but then the numbers change, maybe the value is going up, and they decide to sell in individually?

I see it happening that way as often as I see it happening the other way. The reason why is developers and builders want to maximize their profit. There’s an execution to help them do that. A biller comes in and finds a project. Their initial thought was, “I don’t think I could sell these retail for any number of reasons. It’ll make a good build-to-rent deal.” They buy it and end up developing it. Something happens when interest rates double or more. All of a sudden, the numbers as a build-to-rent don’t make any more sense. It does not work as a build-to-rent.

Very often the builder will say, “I can’t sell it as a build-to-rent. That doesn’t make sense. That’s a bad execution.” I still don’t think I’ll be able to sell in retail At that point, maybe they’ll sell the lots or be able to look back and think, “I can’t sell this build-to-rent. I’m going to land bank it and sit on it for a year until let rates come down.” That’ll be my execution. I’ll figure out if it’s a retail or a build-to-rent play. In my opinion, builders are interested in maximizing what they have on our contract and own. They’ll do any of the above if they think it’ll make them a larger profit and they think it’ll serve the needs of the market. It can be cut both ways.

That’s a beautiful thing about BTR. You have multiple exit plans. Advice to a developer or build-to-rent investor or developer is to reach out to somebody like you early on because then they have access to your brain power for different strategies.

That would be great because it’ll give more conversations. If you’re a builder or developer and you’re looking at projects, always start with the end client in mind and renter. Start looking at projects not as a builder that might look at a land price cost to develop the lots home price, which is generally the equation, “I buy the land for X, a development for Y. I sell the house for Z, make a profit.”

Build To Rent: If you’re a builder or developer looking at a project, always start with the end client in mind.

If you look at it from the perspective of, “What is the profile of the renter that I’m hoping to service with this unit? Are there an abundance of them?” Answer that question first. “What will that renter rent this unit for reasonably?” If you could figure that out, you can pretty easily figure out the rest of the equation because everything else falls in line. That would be my suggestion. Get to know the rental market well and then have that be your starting point.

Let’s move on and make some predictions here. I have my thesis when it comes to build-to-rent or single-family rental communities. I’m more than happy for you to correct me because you’re in this space more than I am. My belief is that our generation, Millennials and the next generations that are coming along, seem to be more of a subscription-based generation like, “This is our income, a portion of it goes to rent and a portion of it goes to eating out.” We’re very much structured in that way. We’re not like our parents or the next generation, maybe like our parents who bought a home and lived there for most of their lives. They seem to be more transitory. They seem to migrate more.

Sometimes people are living in Florida and then Texas. They seem to move a lot. Build-to-rent communities seem to serve these demographics because they know they can rent a nearly new home. They can be part of a rental community where everybody else also rents. They’re not like one renter among all homeowners. They have amenities there. They can move anytime they want. They’re not handcuffed by having a mortgage or living in one place. I feel there’s going to be more and more people living in these communities of single-family homes that are owned by institutions that are publicly traded. It’s going to continue to grow. Do you share that or any part of that? Am I going on the right idea here?

There are certainly swats of people in Millennials especially those who are more mobile and want more options. They don’t want to be tied to one place. Build-to-rent offers a good solution for that. I don’t necessarily agree with the idea that we should turn into a country of renters. Owning a home, at least for me in my experience, is a very important part of building long-term wealth. I hear a lot of financial experts talk about the fact that a home isn’t an investment. It’s true when you think about it from the perspective of you’re losing money on a home. You’re not making money other than the appreciation. It’s costing you money. It’s not necessarily an investment.

I come from a time where my parents, a lot of my friends, and people that I know, the biggest part of their net worth is the equity they built in their home. I don’t think that should change. Anyone who aspires to home ownership is well-founded in doing that. What you’ll end up seeing as the build-to-rent and rental industry moves along is providing some solutions for people who want to build equity in their homes as well. It’s already starting to happen where you can rent with certain companies and also have part of your rent go toward an equity position in the home.

There are platforms that are coming out that if you rent from them, you could also invest in the community that you live in. I am of the mind that people should have the option to not own and be as mobile as they want to and not commit to one place. What I’m teaching my kids is, “When you can afford to buy a home in a place that you like or own a piece of real estate, you should go ahead and buy a piece of real estate because it’s still the best well building tool that’s out there.”

Here’s an idea. Buy a home and live in there as long as you want. When you want to move somewhere else, put it into that rental pool that’s being managed by an institution, and somebody calls can come and live in there. It’s similar to Airbnb but rather communities of single-family homes. It’s an interesting idea.

My friend is like, “When I’m 60, I’d love to have 4 or 5 homes in places I’d like to visit and be the granddad that says, ‘Next week’s open, why don’t we all take all nine of us and go to a house down in Cape Coral?’”

Let’s make some predictions before we get to the next segment of our show here. Seventy percent a year-over-year drop in multifamily transactions. This was 2022 to 2023. What are you seeing in your space? Has it been quite the way multifamily? Has it been worse or better? How was your space over 2022?

Transaction volume, I don’t the exact number but it had to be at least 70% or the same. It’s temporary. It’s a function of interest rates. When interest rates go up, transaction volume goes down because cap rates end up getting decompressed. It creates opportunities for good operators that know how to operate their properties well, buy them well, and can continue to have cashflowing where they don’t have to sell. It’s going to create opportunities for those guys to buy deals from operators that didn’t buy well and don’t operate well and have to sell.

Build To Rent: Transaction volume goes down when interest rates go up because cap rates end up decompressed.

Let’s talk about as far as transactions you’re seeing similar to multifamily, around that 70% mark, how about distress? Are you seeing distress in your space?

I don’t see a whole lot of distress in what I do because I’m generally working with operators that own 10, 20, or 50 single-family properties and they’ve been doing it for 10, 12, or 15 years. I’m working with builders who built rental communities, put tenants in them, and are operating them. I haven’t seen a lot of distress. Is there some in the market? There is but it’s certainly not as easy to find as it was back in 2010.

Distress is everywhere. You throw a rock and hit a property that was going through foreclosure. The opportunity in terms of distress for build-to-rent is looking at developers that develop pieces of property that they’re probably losing money on. They get a loan to buy the property and develop it. They can’t get it sold. They’re bleeding money. How do you find those people? It varies market by market.

There’s an opportunity on the land side because those guys very often are not all that cash-rich. They put a lot of money into a single project and it’s locked up in there. If they’re losing money on it, spending money on insurance, taxes, and a loan, eventually, that stress becomes too much for them and they get into a distressed position where they’re willing to sell for a much lower price.

These are the guys who were doing entitlements, bought the land, and got a shovel ready. That’s the stage where they’re finding themselves in trouble.

Sometimes, I see those guys that are out there. I see builders that are building homes that they expected to sell as a rental portfolio and those rental buyers aren’t buying that product at the right price anymore. They’re sitting on top of vacant properties. They’re losing money on it every single month. They’re either going to rent it out. Some of those buyers didn’t buy or bill for the right prices. They might rent it out and still have negative cashflow, in which case they’re in a stress position a lot less.

It’s not everywhere. It’s more for people that have gone to a bad position where they didn’t buy correctly, they didn’t finance correctly, they underestimated or overestimated the rents or they underestimated how much buyer interest was out there. They are sitting on inventory that’s costing them money and they have to make.

The last question before we get to the next segment of the show is the new question I’d like to ask most of our guests who come in. Real estate is cyclical. I hope that you subscribe to this concept but real estate goes through cycles in my opinion and many experts’ opinion. It’s on that logic that it goes through this cycle. Imagine that cycle as a clock, 12:00 being the top of the market and 6:00 being the bottom of the market. What time is it?

It’s about 10:00. We’re toward the top of the market. The question is how big the dip once it gets to 12:00 or does it dip at all?

6:00 is the bottom.

We’re at 10:00. Here’s a more specific way to say it. We’re shortly out of the bottom of the market. If you consider 2008 to be the bottom of the market, we went way up and hit a little low.

Let’s imagine that was a different cycle. We’re in a new cycle.

We started new cycles. Is it the latter part of 2000?

Let’s say the market started going up in 2011. The bottom was 2010 and 2011. That’s the start of this cycle. The market dipped around 2018 and 2019. We had COVID which gave us the shortest recession ever in history, which was the 3-month recession, and then the rates came down and went hyperbolic from 2020 to 2021.

Maybe I don’t enough about it. You had a run-up in prices for 2009 through 2018. We hit a time when states were stagnant. COVID hit and real estate prices went through the roof.

Initially, it was a bit of a drop. There was an actual recession in the economy for three months. It was the shortest recession ever, which was a tiny dip but then it went on a bull run.

It was a blip but it ended up right after that it went through the river. The prices went up by a dramatic amount. I don’t know how I delineate over the last many years into how many cycles that is because cycle I have looked at home prices since 2009. If you put a line through that, it went straight up. There were a few blips where in 2018, we took a little dip and went right up after that. I don’t know if I consider that more than one cycle.

The prices have come down since 2000 and 2021. In multifamily, prices have been down a bit.

Prices have gone up and the value of a home in 2024 is more than it was in 2023. There was never a point year to year where home prices didn’t go up. At least residential housing prices didn’t go up. When I look at the housing chart, I see nothing but a run-up in housing prices from the turn of the decade. We had little blips in that but even throughout the course of time where interest rates were going up in the residential housing market, home prices consistently went up year over year.

We’re toward the top end of the market. We’re not at the bottom. I don’t think prices have a whole huge amount to run at a price level where people can’t afford to buy at a higher price. We’re going to flatten out a little bit. The same thing’s probably going to happen with rental rates, which is probably the reason why build-to-rent deals are so much harder to pencil in.

A lot of people generally err on the side of caution thinking the same thing. “How much can you without wage growth improving a whole lot? How much higher can you push rental rates or how much higher can you push home rates where people aren’t going to be able to afford them anymore?” That drives my opinion of why we’re probably not at the top of the market but toward the top end of the market.

We're not at the top of the market but are toward the top. The market is looking interesting. Click To TweetIt’s interesting you say that because some scholars are saying that there is a serious recession coming to the US real estate market in 2026 and 2027. That aligns with that concept being 10:00 or 12:00 top of the market, which goes down from there. Let’s get to the next segment.

Thank you for being such an amazing guest. We’re excited about the next segment here. It’s called The Ten Championship Rounds to Financial Freedom. Whatever comes top of mind. The first question is this. Who’s been the most influential person in your life?

It sounds corny and a lot of busy people might not agree with me but my wife’s been the most influential person in my life. The center of my life is family, my kids, and my home life. It drives every single thing that I do. If I can think of one person who has had a bigger effect on me than my wife in building the life we had together, it would be her.

If I were going to talk about business-wise, I wouldn’t name names because there are a few of them but I’ve had people I’ve met through transactions whom I ended up becoming good friends with. I’ve learned a lot from them in the way they look at money and how they built their wealth over time. A lot of those are medium-sized real estate investors. It’s probably a dozen of them. I get as much from each one as I do from the other. That’s where I get my inspiration from. People I end up doing transactions with, I end up learning a lot from them as business people.

Most of our guests are scared of their wives. They’ll always say the wife.

In my case, it is true.

The next question is, what is the number one book you would recommend?

There’s a lot. I’m reading a book called The Long Slide by Tucker Carlson. It’s a book where he talks about his last 30 years in journalism and how corrupt the media establishment has gotten in the interests that are guiding what people report on and how they report it.

The Long Slide: Thirty Years in American Journalism

I’ve watched them being ultra-right drinking the Kool-Aid when it comes to a lot of ideas and then not going otherwise. It is open-minded. He openly discusses it. I enjoyed listening to him and the man he’s become. He’s so transparent about the journey he’s taken. I would be looking forward to that book.

He tells it in little snippets stories from his early years as an assistant in the publishing industry to when it became the Tucker Carlson we knew, the stories and the people he met all along the way, and publishing has generally gotten corrupt, and how special interests are driving the whole publishing industry. It was an interesting take from a guy who’s been an insider for the last 30 years.

Next question, if you had the opportunity to travel back in time, what advice would you give your younger self?

The first thing is it doesn’t matter how much money you put aside but put a little bit more aside every single month into something. It doesn’t matter if it’s index funds and stocks or whether it’s a bank account but do it more consistently than you did it because it doesn’t matter if it’s even $200 or $100. Don’t go even a week or a month without putting something aside every time you make money. That’s the biggest thing I tell myself. Save more money and put it into cashflowing or appreciating assets.

It doesn't matter how much money you put aside. Put a little bit more every month into something that doesn't matter. Do it more consistently than you did it because it doesn't matter. Click To TweetGoogle compounding interest, that explains it right there.

The other thing is I go back to myself in 2009 and I’d say, “Don’t do what you’re thinking about doing. Move to Phoenix, Vegas, Atlanta, or Charlotte, figure out how to buy properties, go raise a little bit of money for your family and friends, and buy as many properties as you can.”

We go over that story all the time, buying in Phoenix.

Next question, what’s the best investment you’ve ever made?

It was a building in my town that I ended up making my office. I bought it. It was a vacant flex space. I ended up putting my team in there for a little while and renting it out. It’s been a great cashflow investment. It’s appreciated well.

What’s the worst investment you’ve ever made? What lessons did you learn from it?

The worst investment I ever made was a house that I bought that was too far away from my house. I didn’t understand the neighborhood. It was a pain in the ass to manage. I couldn’t stand it anymore and I sold it for less than I bought it for a couple of years later.

Next question, how much would you need in the bank to retire? What’s your number?

$5 million. There are two parts to that question. If I had to have money to live the life I want to live, not work anymore, and have a reason to not work, I feel like $5 million gets me everything and gets me the FU money that I would need to be happy. Otherwise, I’d probably start working again. The amount of money I need to survive in the bank, I don’t know, I’m a pretty reasonable guy. $1 million? I can put that to work and live on $60,000 a year.

How much would you need in the bank to retire today? What’s your number?

I’d have to do some research but I want to figure out what my nut is. I know the number. The least risky investment I can make with the principal amount is that stack of money invested in a safe asset that throws up enough cash flow to pay my bills. That much money.

Know the number and the least risky investment with the principal amount, and that's the exact amount of money invested in a safe asset that throws up enough cash flow to pay your bills. Click To TweetLeave all the passive income.

That was our trick question, does it cashflow?

You have that much money, probably only a couple of million at the end of the day.

If you could have dinner with someone dead or alive, who would it be?

I would have dinner with Abraham Lincoln. If it was more contemporary, I wouldn’t mind having dinner with Joe Rogan on his podcast.

If you weren’t doing what you’re doing now, what would you be doing?

I’d like to try my hand at a couple of things but what I’d probably like to try my hand at is something with my hands. If my ego got in the way and I could make money in what I’m doing, building things would be rewarding for me because I’m in an industry where my work disappears after a little while. I don’t have anything that’s concrete that can hold my hands. I’d love to learn how to learn a trade and use my hands to build things.

Build To Rent: Learn a trade and use your hands to build things.

Two more questions left. Book smarts or street smarts?

Street smarts all the way.

Last question. If you had $1 million in cash and you had to make one investment, what would it be?

I kicked myself for not doing this and it was $1 million in cash. It was an investment that I love to make. I ride it because it would be an interesting investment to make. There are a bunch of cryptocurrencies out there that are doing some cool things with the currency being used by different companies and corporations for very specific projects in very specific sectors. I’d pick one of a few cryptocurrencies that apply to a sector that has good growth opportunities.

It’ll be the thing where I either don’t make any money, I lose all my money, or I see a 30X return. I’ve never invested in cryptocurrencies because I don’t have the stomach for it but if I had $1 million and I got to take the investment that I would most like to do, I’d like to research some of those cryptocurrencies and probably make an investment in them.

You get the highest returns if it hits but coming from a guy who did invest in them, if you’ve got to invest in cryptocurrencies, do Bitcoin and leave it there. Don’t invest in anything else. We appreciate it. Thank you so much for being on our show. We learned a lot like usual lot. Please let our audience know what’s the best way they can reach out to you.

It’s easy. You go to www.StrataSFR.com. I’m easy enough to find.

Thank you so much, Adam.

This has been great. I appreciate you having me on.