In private equity investment, a cap rate spread is a very important metric in all real estate transactions. As most investors know, many of the key metrics used to endeavour to measure the performance of investments are interlinked, with the relationship between cap rates and interest rates being one of the most watched.

Just to be sure, what is a cap rate?

We have discussed cap rates previously but it’s worth taking a few moments to again review the basic premise of such a metric to help gain a better insight into cap rate spread.

The capitalisation rate (“cap rate”) is a performance based metric which describes the relationship between a property’s net operating income (“NOI”) and its estimated current market value..

The formula used to calculate it is: Net Operating Income / Property Value.

Basically, real estate investors calculate NOI by subtracting operating expenses from total income and the result provides some insight into the property’s operational efficiency.

A lower cap rate generally means that the property is considered to have less risk, which invariably means steady, reliable growth in cash flow. This means that properties such as multi-family apartments or those with financially strong tenants have the lowest cap rates.

At the other end of the spectrum, higher cap rates mean that the property is perceived to have more risk and, therefore, investors expect a higher rate of return and, accordingly, a lower price. Properties in riskier asset classes include hotels, restaurants and office buildings or those which have higher vacancy rates or operational issues and these tend to display higher cap rates.

Important pieces of information gleaned by investors from cap rates

When investors are evaluating a potential PERE transaction, the cap rate provides investors with two important pieces of information:

- an indication of the annual rate of return assuming the property is purchased with cash. There are a variety of factors which affect cap rates and these include potential rental growth rates, the level and likely growth of operating expenses, liquidity and tenant leasing activity and vacancy rates;

- an indication of the market’s assessment of the risk associated with the property. As mentioned above, higher cap rates indicate higher risk (higher returns) and lower cap rates mean less risk (less risk).

What is the cap rate spread?

The cap rate spread is a metric which attempts to identify risk and can be defined as the difference between the interest rate on the 10-Year Treasury note and the cap rate of a transaction.

The calculation of the spread is straightforward and represents a very important indicator about return expectations of an investment.

The cap rate spread can be explained as follows: if, for example, a real estate investor purchases a 10-year Treasury note, in essence they are making a loan of the amount paid for the note to the US government. Naturally, an investor will expect to have their investment returned plus the relevant interest when the term of the note expires. is up. Such a “loan” is considered to be as risk free as an investment can be and, accordingly, the interest rate on the 10-year Treasury is generally referred to as the “risk free rate.”

On the other hand, the cap rate represents the annual return on a CRE investment, assuming it was purchased with cash. Because commercial real estate assets attract more risk than a 10-year Treasury note, it stands to reason that an investor should seek to earn a higher rate of return.

In view of the foregoing, the cap rate spread can be defined as the difference between the interest rate on the 10-year Treasury note and the prevailing cap rate for a property. In other words, it represents an investor’s compensation for purchasing a real estate asset and not a Treasury note.

As an example, if an investor acquires a multi-family apartment property at a 6.5% cap rate when the interest rate on a 10 year Treasury note is 2%, the “spread” of 4.5% or 450 basis points represents the compensation an investor will seek for the additional risk of purchasing an investment property over the note.

[ Passive investors : do you know how to vet a real estate investment group before making an investment?

Download and read our FREE e-book: 25 Fundamental questions to ask a Syndication Sponsor before making your investment. ]

Why is the cap rate spread important in CRE investment?

The yields on 10-year Treasury notes are not the same day to day and move with market demand and supply, plus other external factors.

Cap rates tend to track movements in Treasury note rates although movements do not correlate directly. The difference or spread between the two can expand and contract based on both macro- and micro-economic conditions.

Fundamentally, in times of economic uncertainty, real estate investors tend to prefer the relative safety of Treasuries so the cap rate spread widen yet conversely in times of economic growth, investors feel more amenable to risk so tend to sell Treasuries, which drives rates up and compresses the cap rate spread.

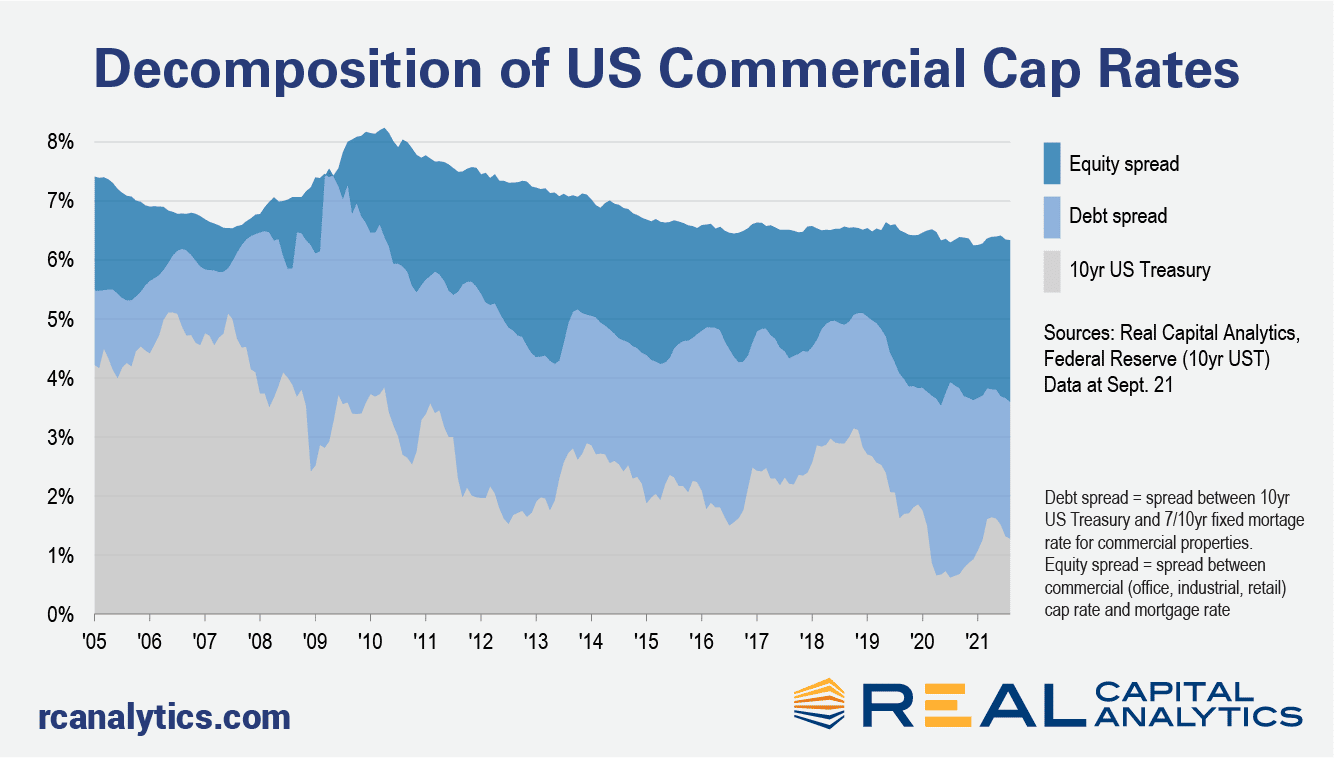

The following chart illustrates this point

The above chart shows the 10-year Treasury note rate compared with average cap rates for various CRE property types over the last 20 years or so.

During the years of the Global Financial Crisis (“GFC”) 10-year Treasury rates declined while CRE cap rates rose causing the spread to increase. The chart also shows the spread for various property types, for example, multi-family being more stable so the spread is lower. On the other hand, higher risk assets such as office buildings and hotels invariably have higher risk so the spread is wider.

It can be seen that as economic recovery takes shape from around 2010 onwards, Treasury note yields stay relatively stable whereas property cap rates rise significantly, causing asset values to rise and narrowing the cap rate spread.

With its vast experience in PERE transactions, CPI Capital understands that the cap rate spread in CRE is important as it provides investors with information about the future direction of property prices and risk expectations. Generally, when the spread is wide or widening, it indicates a riskier investment environment, one key reason that compensation must be higher than Treasuries. When the spread is narrow or narrowing, economic market conditions are much more stable so investors are prepared to accept a lower return for the incremental risk over Treasuries.

We also know that information about the relationship between cap rates and Treasuries should always be used in the underwriting process to help assess the appropriate purchase price in an investment transaction as they can have a significant impact on a property’s profitability.

Of course, maximising the investment returns for our passive investors remains as our key focus, so the cap rate spread is always closely watched!

Yours sincerely,

August Biniaz

Ready to build true wealth for your family?

It all starts with passive income. Apply to join the CPI Capital Investor Club.

Search

Recommended

What is the Correlation Between Bond Yields and Real Estate Cap Rates?

Dear valued existing investors and future investors, Welcome to CPI Capital's regular news...

The Sunk Cost Fallacy In Active Real Estate Investing: Embracing The Power of Multifamily Syndications

Dear valued existing investors and future investors, Welcome to this week's CPI Capital's news...

Key Metrics Every Multifamily Investor Needs to Know

Dear valued existing investors and future investors, Welcome once again to this week’s CPI...